- 4. Expectation

- 4.1 Expectation of a Random Variable

- 4.2 Properties of Expectations

- 4.3 Variance and Covariance

- 4.4 Expectation and Variance of Important Random Variables

- 4.5 Conditional Expectation

- 4.6 Technical Appendix

- 4.7 Exercises

- 4.8 Negative binomial (or gamma-Poisson) distribution and gene expression counts modeling

- 4.9 Beta distribution and Order Statistics

- 4.10 The conditional log-likelihood (CML) of NB distribution

- References

4. Expectation

4.1 Expectation of a Random Variable

The expected value, mean or first moment of \(X\) is defined to be

\[ \mathbb{E}(X) = \int x \; dF(x) = \begin{cases} \sum_x x f(x) &\text{if } X \text{ is discrete} \\ \int x f(x)\; dx &\text{if } X \text{ is continuous} \end{cases} \]

assuming that the sum (or integral) is well-defined. We use the following notation to denote the expected value of \(X\):

\[ \mathbb{E}(X) = \mathbb{E}X = \int x\; dF(x) = \mu = \mu_X \]

The expectation is a one-number summary of the distribution. Think of \(\mathbb{E}(X)\) as the average value you’d obtain if you computed the numeric average \(n^{-1} \sum_{i=1}^n X_i\) for a large number of IID draws \(X_1, \dots, X_n\). The fact that \(\mathbb{E}(X) \approx n^{-1} \sum_{i=1}^n X_i\) is a theorem called the law of large numbers which we will discuss later. We use \(\int x \; dF(x)\) as a convenient unifying notation between the discrete case \(\sum_x x f(x)\) and the continuous case \(\int x f(x) \; dx\) but you should be aware that \(\int x \; dF(x)\) has a precise meaning discussed in real analysis courses.

To ensure that \(\mathbb{E}(X)\) is well defined, we say that \(\mathbb{E}(X)\) exists if \(\int_x |x| \; dF_X(x) < \infty\). Otherwise we say that the expectation does not exist. From now on, wheneverwe discuss expectations, we implicitly assume they exist.

Theorem 4.6 (The rule of the lazy statician). Let \(Y = r(X)\). Then

\[ \mathbb{E}(Y) = \mathbb{E}(r(X)) = \int r(x) \; dF_X(x) \]

As a special case, let \(A\) be an event and let \(r(x) = I_A(x)\), where \(I_A(x) = 1\) if \(x \in A\) and \(I_A(x) = 0\) otherwise. Then

\[ \mathbb{E}(I_A(X)) = \int I_A(x) f_X(x) dx = \int_A f_X(x) dx = \mathbb{P}(X \in A) \]

In other words, probability is a special case of expectation.

Functions of several variables are handled in a similar way. If \(Z = r(X, Y)\) then

\[ \mathbb{E}(Z) = \mathbb{E}(r(X, Y)) = \int \int r(x, y) \; dF(x, y) \]

The \(k\)-th moment of \(X\) is defined to be \(\mathbb{E}(X^k)\), assuming that \(\mathbb{E}(|X|^k) < \infty\). We shall rarely make much use of moments beyond \(k = 2\).

4.2 Properties of Expectations

Theorem 4.10. If \(X_1, \dots, X_n\) are random variables and \(a_1, \dots, a_n\) are constants, then

\[ \mathbb{E}\left( \sum_i a_i X_i \right) = \sum_i a_i \mathbb{E}(X_i) \]

Theorem 4.12. Let \(X_1, \dots, X_n\) be independent random variables. Then,

\[ \mathbb{E}\left(\prod_i X_i \right) = \prod_i \mathbb{E}(X_i) \]

Notice that the summation rule does not require independence but the product does.

4.3 Variance and Covariance

Let \(X\) be a random variable with mean \(\mu\). The variance of \(X\) – denoted by \(\sigma^2\) or \(\sigma_X^2\) or \(\mathbb{V}(X)\) or \(\mathbb{V}X\) – is defined by

\[ \sigma^2 = \mathbb{E}(X - \mu)^2 = \int (x - \mu)^2\; dF(x) \]

assuming this expectation exists. The standard deviation is \(\text{sd}(X) = \sqrt{\mathbb{V}(X)}\) and is also denoted by \(\sigma\) and \(\sigma_X\).

Theorem 4.14. Assuming the variance is well defined, it has the following properties:

\(\mathbb{V}(X) = \mathbb{E}(X^2) - \mathbb{E}(X)^2\)

If \(a\) and \(b\) are constants then \(\mathbb{V}(aX + b) = a^2 \mathbb{V}(X)\)

If \(X_1, \dots, X_n\) are independent and \(a_1, \dots, a_n\) are constants then

\[ \mathbb{V}\left( \sum_{i=1}^n a_iX_i \right) = \sum_{i=1}^n a_i^2 \mathbb{V}(X_i) \]

If \(X_1, \dots, X_n\) are random variables then we define the sample mean to be

\[ \overline{X}_n = \frac{1}{n} \sum_{i=1}^n X_i \]

and the sample variance to be

\[ S_n^2 = \frac{1}{n - 1} \sum_{i=1}^n \left(X_i - \overline{X}_n\right)^2 \]

Theorem 4.16. Let \(X_1, \dots, X_n\) be IID and let \(\mu = \mathbb{E}(X_i)\), \(\sigma^2 = \mathbb{V}(X_i)\). Then

\[ \mathbb{E}\left(\overline{X}_n\right) = \mu, \quad \mathbb{V}\left(\overline{X}_n\right) = \frac{\sigma^2}{n}, \quad \text{and} \quad \mathbb{E}\left(S_n^2\right) = \sigma^2 \]

If \(X\) and \(Y\) are random variables, then the covariance and correlation between \(X\) and \(Y\) measure how strong the linear relationship between \(X\) and \(Y\) is.

Let \(X\) and \(Y\) be random variables with means \(\mu_X\) and \(\mu_Y\) and standard deviation \(\sigma_X\) and \(\sigma_Y\). Define the covariance between \(X\) and \(Y\) by

\[ \text{Cov}(X, Y) = \mathbb{E}[(X - \mu_X)(Y - \mu_Y)] \]

and the correlation by

\[ \rho = \rho_{X, Y} = \rho(X, Y) = \frac{\text{Cov}(X, Y)}{\sigma_X \sigma_Y} \]

Theorem 4.18. The covariance satisfies:

\[ \text{Cov}(X, Y) = \mathbb{E}(XY) - \mathbb{E}(X) \mathbb{E}(Y) \]

The correlation satisfies:

\[ -1 \leq \rho(X, Y) \leq 1 \]

If \(Y = a + bX\) for some constants \(a\) and \(b\) then \(\rho(X, Y) = 1\) if \(b > 0\) and \(\rho(X, Y) = -1\) if \(b < 0\). If \(X\) and \(Y\) are independent, then \(\text{Cov}(X, Y) = \rho = 0\). The converse is not true in general.

Theorem 4.19.

\[ \mathbb{V}(X + Y) = \mathbb{V}(X) + \mathbb{V}(Y) + 2 \text{Cov}(X, Y) \quad \text{ and } \quad \mathbb{V}(X - Y) = \mathbb{V}(X) + \mathbb{V}(Y) - 2 \text{Cov}(X, Y) \]

More generally, for random variables \(X_1, \dots, X_n\),

\[ \mathbb{V}\left( \sum_i a_i X_i \right) = \sum_i a_i^2 \mathbb{V}(X_i) + 2 \sum \sum_{i < j} a_i a_j \text{Cov}(X_i, X_j) \]

4.4 Expectation and Variance of Important Random Variables

\[ \begin{array}{lll} \text{Distribution} & \text{Mean} & \text{Variance} \\ \hline \text{Point mass at } p & a & 0 \\ \text{Bernoulli}(p) & p & p(1-p) \\ \text{Binomial}(n, p) & np & np(1-p) \\ \text{Negative binomial}(r,p) & \frac{r(1-p)}{p} & \frac{r(1-p)}{p^2} \text{ Or } \mu+\frac{1}{r}\mu^2\\ \text{Geometric}(p) & \begin{cases} 1/p,& (k=1,2,3,\cdots) \\ \frac{1-p}{p},& (k=0, 1,2,\cdots) \end{cases} & (1 - p)/p^2 \\ \text{Cauchy} & \infty & \infty \\ \text{Poisson}(\lambda) & \lambda & \lambda \\ \text{Uniform}(a, b) & (a + b) / 2 & (b - a)^2 / 12 \\ \text{Normal}(\mu, \sigma^2) & \mu & \sigma^2 \\ \text{Exponential}(\beta) & \beta & \beta^2 \\ \text{Gamma}(\alpha, \beta) & \alpha \beta & \alpha \beta^2 \\ \text{Inverse-Gamma}(\alpha, \beta) & \frac{1}{(\alpha-1)\beta} & \frac{1}{(\alpha-1)^2(\alpha-2)\beta^2} \\ \text{Beta}(\alpha, \beta) & \alpha / (\alpha + \beta) & \alpha \beta / ((\alpha + \beta)^2 (\alpha + \beta + 1)) \\ t_\nu & 0 \text{ (if } \nu > 1 \text{)} & \nu / (\nu - 2) \text{ (if } \nu > 2 \text{)} \\ \chi^2_k & k & 2k \\ \text{non-central }\chi^2_{k,\lambda} & k+\lambda &2(k+2\lambda) \\ \text{Inverse }\chi^2 &\frac{1}{k-2}\quad (k>2) & \frac{2}{(k-2)^2(k-4)} \quad (k>4)\\ \text{Multinomial}(n, p) & np & \text{see below} \\ \text{Multivariate Nornal}(\mu, \Sigma) & \mu & \Sigma \\ \text{Logistic}(\mu, s) & \mu & \frac{s^2\pi^2}{3} \\ \end{array} \]

The last two entries in the table are multivariate models which involve a random vector \(X\) of the form

\[ X = \begin{pmatrix} X_1 \\ \vdots \\ X_k \end{pmatrix} \]

The mean of a random vector \(X\) is defined by

\[ \mu = \begin{pmatrix} \mu_1 \\ \vdots \\ \mu_k \end{pmatrix} = \begin{pmatrix} \mathbb{E}(X_1) \\ \vdots \\ \mathbb{E}(X_k) \end{pmatrix} \]

The variance-covariance matrix \(\Sigma\) is defined to be

\[ \Sigma = \begin{pmatrix} \mathbb{V}(X_1) & \text{Cov}(X_1, X_2) & \cdots & \text{Cov}(X_1, X_k) \\ \text{Cov}(X_2, X_1) & \mathbb{V}(X_2) & \cdots & \text{Cov}(X_2, X_k) \\ \vdots & \vdots & \ddots & \vdots \\ \text{Cov}(X_k, X_1) & \text{Cov}(X_k, X_2) & \cdots & \mathbb{V}(X_k) \end{pmatrix} \]

If \(X \sim \text{Multinomial}(n, p)\) then

\[ \mathbb{E}(X) = np = n(p_1, \dots, p_k) \quad \text{and} \quad \mathbb{V}(X) = \begin{pmatrix} np_1(1 - p_1) & -np_1p_2 & \cdots & np_1p_k \\ -np_2p_1 & np_2(1 - p_2) & \cdots & np_2p_k \\ \vdots & \vdots & \ddots & \vdots \\ -np_kp_1 & -np_kp_2 & \cdots & np_k(1 - p_k) \end{pmatrix} \]

To see this:

- Note that the marginal distribution of any one component is \(X_i \sim \text{Binomial}(n, p_i)\), so \(\mathbb{E}(X_i) = np_i\) and \(\mathbb{V}(X_i) = np_i(1 - p_i)\).

- Note that, for \(i \neq j\), \(X_i + X_j \sim \text{Binomial}(n, p_i + p_j)\), so \(\mathbb{V}(X_i + X_j) = n(p_i + p_j)(1 - (p_i + p_j))\).

- Using the formula for the covariance of a sum, for \(i \neq j\),

\[ \mathbb{V}(X_i + X_j) = \mathbb{V}(X_i) + \mathbb{V}(X_j) + 2 \text{Cov}(X_i, X_j) = np_i(1 - p_i) + np_j(1 - p_j) + 2 \text{Cov}(X_i, X_j) \]

Equating the last two formulas we get a formula for the covariance, \(\text{Cov}(X_i, X_j) = -np_ip_j\).

Finally, here’s a lemma that can be useful for finding means and variances of linear combinations of multivariate random vectors.

Lemma 4.20. If \(a\) is a vector and \(X\) is a random vector with mean \(\mu\) and variance \(\Sigma\) then

\[ \mathbb{E}(a^T X) = a^T \mu \quad \text{and} \quad \mathbb{V}(a^T X) = a^T \Sigma a \]

If \(A\) is a matrix then

\[ \mathbb{E}(A X) = A \mu \quad \text{and} \quad \mathbb{V}(AX) = A \Sigma A^T \]

4.5 Conditional Expectation

The conditional expectation of \(X\) given \(Y = y\) is

\[ \mathbb{E}(X | Y = y) = \begin{cases} \sum x f_{X | Y}(x | y) &\text{ discrete case} \\ \int x f_{X | Y}(x | y) dy &\text{ continuous case} \end{cases} \]

If \(r\) is a function of \(x\) and \(y\) then

\[ \mathbb{E}(r(X, Y) | Y = y) = \begin{cases} \sum r(x, y) f_{X | Y}(x | y) &\text{ discrete case} \\ \int r(x, y) f_{X | Y}(x | y) dy &\text{ continuous case} \end{cases} \]

While \(\mathbb{E}(X)\) is a number, \(\mathbb{E}(X | Y = y)\) is a function of \(y\). Before we observe \(Y\), we don’t know the value of \(\mathbb{E}(X | Y = y)\) so it is a random variable which we denote \(\mathbb{E}(X | Y)\). In other words, \(\mathbb{E}(X | Y)\) is the random variable whose value is \(\mathbb{E}(X | Y = y)\) when \(Y\) is observed as \(y\). Similarly, \(\mathbb{E}(r(X, Y) | Y)\) is the random variable whose value is \(\mathbb{E}(r(X, Y) | Y = y)\) when \(Y\) is observed as \(y\).

Theorem 4.23 (The rule of iterated expectations). For random variables \(X\) and \(Y\), assuming the expectations exist, we have that

\[ \mathbb{E}[\mathbb{E}(Y | X)] = \mathbb{E}(Y) \quad \text{and} \quad \mathbb{E}[\mathbb{E}(X | Y)] = \mathbb{E}(X) \]

More generally, for any function \(r(x, y)\) we have

\[ \mathbb{E}[\mathbb{E}(r(X, Y) | X)] = \mathbb{E}(r(X, Y)) \quad \text{and} \quad \mathbb{E}[\mathbb{E}(r(X, Y) | Y)] = \mathbb{E}(r(X, Y)) \]

Proof. We will prove the first equation.

\[ \begin{align} \mathbb{E}[\mathbb{E}(Y | X)] &= \int \mathbb{E}(Y | X = x) f_X(x) dx = \int \int y f(y | x) dy f(x) dx \\ &= \int \int y f(y|x) f(x) dx dy = \int \int y f(x, y) dx dy = \mathbb{E}(Y) \end{align} \]

The conditional variance is defined as

\[ \mathbb{V}(Y | X = x) = \int (y - \mu(x))^2 f(y | x) dx \]

where \(\mu(x) = \mathbb{E}(Y | X = x)\).

Theorem 4.26. For random variables \(X\) and \(Y\),

\[ \mathbb{V}(Y) = \mathbb{E}\mathbb{V}(Y | X) + \mathbb{V} \mathbb{E} (Y | X)\]

4.6 Technical Appendix

4.6.1 Expectation as an Integral

The integral of a measurable function \(r(x)\) is defined as follows. First suppose that \(r\) is simple, meaning that it takes finitely many values \(a_1, \dots, a_k\) over a partition \(A_1, \dots, A_k\). Then \(\int r(x) dF(x) = \sum_{i=1}^k a_i \mathbb{P}(r(X) \in A_i)\). The integral of a positive measurable function \(r\) is defined by \(\int r(x) dF(x) = \lim_i \int r_i(x) dF(x)\), where \(r_i\) is a sequence of simple functions such that \(r_i(x) \leq r(x)\) and \(r_i(x) \rightarrow r(x)\) as \(i \rightarrow \infty\). This does not depend on the particular sequence. The integral of a measurable function \(r\) is defined to be \(\int r(x) dF(x) = \int r^+(x) dF(x) - \int r^-(x) dF(x)\) assuming both integrals are finite, where \(r^+(x) = \max \{ r(x), 0 \}\) and \(r^-(x) = \min\{ r(x), 0 \}\).

4.6.2 Moment Generating Functions

The moment generating function (mgf) or Laplace transform of \(X\) is defined by

\[ \psi_X(t) = \mathbb{E}(e^{tX}) = \int e^{tx} dF(x) \]

where \(t\) varies over the real numbers.

In what follows, we assume the mgf is well defined for all \(t\) in small neighborhood of 0. A related function is the characteristic function, defined by \(\mathbb{E}(e^{itX})\) where \(i = \sqrt{-1}\). This function is always defined for all \(t\). The mgf is useful for several reasons. First, it helps us compute the moments of a distribution. Second, it helps us find the distribution of sums of random variables. Third, it is used to prove the central limit theorem.

When the mgf is well defined, it can be shown that we can interchange the operations of differentiation and “taking expectation”. This leads to

\[ \psi'(0) = \left[ \frac{d}{dt} \mathbb{E} e^{tX} \right]_{t = 0} = \mathbb{E} \left[ \frac{d}{dt} e^{tX} \right]_{t = 0} = \mathbb{E}[X e^{tX}]_{t = 0} = \mathbb{E}(X) \]

By taking further derivatives we conclude that \(\psi^{(k)}(0) = \mathbb{E}(X^k)\). This gives us a method for computing the moments of a distribution.

Lemma 4.30. Properties of the mgf.

- If \(Y = aX + b\) then \[ \psi_Y(t) = e^{bt} \psi_X(at) \]

- if \(X_1, \dots, X_n\) are independent and \(Y = \sum_i X_i\) then \(\psi_Y(t) = \prod_i \psi_{i}(t)\), where \(\psi_i\) is the mgf of \(X_i\).

Theorem 4.32. Let \(X\) and \(Y\) be random variables. If \(\psi_X(t) = \psi_Y(t)\) for all \(t\) in an open interval around 0, then \(X \overset{d}= Y\).

Moment Generating Function for Some Common Distributions

\[ \begin{array}{ll} \text{Distribution} & \text{mgf} \\ \hline \text{Geometric}(p) &\frac{pe^t}{1-(1 - p)e^t} \quad k\in\{1,2,3,\cdots\} \quad\text {or}\quad \frac{p}{1-(1 - p)e^t} \quad k\in\{0,1,2,3,\cdots\} \\ \text{Bernoulli}(p) & pe^t + (1 - p) \\ \text{Binomial}(n, p) & (pe^t + (1 - p))^n \\ \text{Poisson}(\lambda) & e^{\lambda(e^t - 1)} \\ \text{Exponential}(\beta) & \frac{1}{1-\beta t} \quad (t-\frac{1}{\beta}<0)\\ \text{Gamma}(\alpha,\beta) & \left(\frac{1}{1-\beta t}\right)^{\alpha} \quad (t-\frac{1}{\beta}<0)\\ \text{standard Normal}(0, 1) & \exp\left(\frac{t^2}{2} \right) \\ \text{Normal}(\mu, \sigma^2) & \exp\left(\mu t + \frac{\sigma^2 t^2}{2} \right) \\ \chi^2(k) & \left(\frac{1}{1-2 t}\right)^{k/2}\quad(t<\frac{1}{2}) \\ \text{non-central }\chi^2(k,\lambda) & \exp\left(\frac{\lambda t}{1-2t}\right)\left(\frac{1}{1-2 t}\right)^{k/2}\quad (2t<1)\\ \text{Logistic}(\mu, s)& e^{\mu t}B(1-st, 1+st)\quad t\in(-1/s,1/s)\\ \end{array} \]

Geometric \[M(t)=\mathbb E[e^{tX}]=\sum_{k=1}^{\infty}e^{tk}p(1-p)^{k-1}\\ =pe^t\sum_{k=1}^{\infty}e^{t(k-1)}(1-p)^{k-1}=pe^t\frac{1}{1-e^t(1-p)}\\ \quad k\in\{1,2,3,\cdots\}\\ \text{and}\quad e^t(1-p)<1\]

\[M(t)=\sum_{k=0}^{\infty}e^{tk}p(1-p)^{k}=p\sum_{k=0}^{\infty}e^{tk}(1-p)^{k}=\frac{p}{1-e^t(1-p)}\\ \quad k\in\{0,1,2,3,\cdots\}\\ \text{and}\quad e^t(1-p)<1\]

Binomial \[\begin{align} M(t)&=\mathbb E[e^{tX}]\\ &=\sum_{k=0}^{n}e^{tk}{n\choose k}p^k(1-p)^{n-k}\\ &=\sum_{k=0}^{n}{n\choose k}(e^{t}p)^k(1-p)^{n-k}\\ &=[pe^{t}+(1-p)]^n \end{align}\]

Poisson \[\begin{align} M(t)&=\mathbb E[e^{tX}]\\ &=\sum_{x=0}^{\infty}e^{tx}\frac{\lambda^x e^{-\lambda}}{x!}\\ &=e^{-\lambda}\sum_{x=0}^{\infty}\frac{(\lambda e^t)^x}{x!}\\ &=e^{-\lambda}e^{\lambda e^t}\\ &=e^{\lambda (e^t-1)}\\ \end{align}\]

Exponential \[\begin{align} M(t)&=\mathbb E[e^{tX}]\\ &=\int_{0}^{\infty}e^{tx}\frac{1}{\beta}e^{-\frac{1}{\beta}x}dx\\ &=\frac{1}{\beta}\int_{0}^{\infty}e^{(t-\frac{1}{\beta})x}dx\\ &=\frac{1}{\beta}\frac{1}{t-\frac{1}{\beta}}(-1)\quad (t-\frac{1}{\beta}<0)\\ &=\frac{1}{1-\beta t} \end{align}\]

Gamma \[\begin{align} M(t)&=\mathbb E[e^{tX}]\\ &=\int_{0}^{\infty}e^{tx}\frac{1}{\Gamma(\alpha)\beta^{\alpha}}e^{-\frac{x}{\beta}}x^{\alpha-1}dx\\ &=\int_{0}^{\infty}\frac{1}{\Gamma(\alpha)\beta^{\alpha}}e^{-(\frac{1}{\beta}-t)x}x^{\alpha-1}dx\\ &=\frac{1}{\Gamma(\alpha)\beta^{\alpha}}\int_{0}^{\infty}e^{-(\frac{1}{\beta}-t)x}x^{\alpha-1}dx\\ &=\frac{1}{\Gamma(\alpha)\beta^{\alpha}}\frac{\Gamma(\alpha)}{(\frac{1}{\beta}-t)^{\alpha}}\\ &=\left(\frac{1}{1-\beta t}\right)^{\alpha}\\ \end{align}\]

standard Normal \[\begin{align} M(t)&=\mathbb E[e^{tz}]\\ &=\int e^{tz}\frac{1}{\sqrt{2\pi}}e^{-\frac{1}{2}z^2}dz\\ &=\frac{1}{\sqrt{2\pi}}\int \exp\left(tz-\frac{1}{2}z^2\right)dz\\ &=\frac{1}{\sqrt{2\pi}}\int \exp\left(-\frac{1}{2}(z-t)^2\right)\exp\left(\frac{1}{2}t^2\right)dz\\ &=e^{\frac{1}{2}t^2}\frac{1}{\sqrt{2\pi}}\int \exp\left(-\frac{1}{2}(z-t)^2\right)dz\\ &=e^{\frac{1}{2}t^2} \end{align}\]

Normal \[\begin{align} M(t)&=\mathbb E[e^{tx}]\\ &=\int e^{tx}\frac{1}{\sqrt{2\pi}\sigma}e^{-\frac{1}{2}(x-\mu)^2/\sigma^2}dx\\ &=\int e^{t(z\sigma+\mu)}\frac{1}{\sqrt{2\pi}}e^{-\frac{1}{2}z^2}dz\\ &=e^{\mu t}\int e^{z\sigma t}\frac{1}{\sqrt{2\pi}}e^{-\frac{1}{2}z^2}dz\\ &=e^{\mu t}e^{\frac{1}{2}\sigma^2t^2}\\ \end{align}\] The final equality follows in view of the final equality of the equation above where the dummy variable \(t\) can be replace by \(\sigma t\).

\(\chi^2\) Since \(\chi^2\) is a \(\Gamma(k/2,2)\) then \[\begin{align} M(t)&=\mathbb E[e^{tX}]\\ &=\int_{0}^{\infty}e^{tx}\frac{1}{\Gamma(k/2)2^{k/2}}e^{-\frac{x}{2}}x^{k/2-1}dx\\ &=\left(\frac{1}{1-2 t}\right)^{k/2}\quad(t<\frac{1}{2})\\ \end{align}\]

non-central chi-squared distribution Let \(Z\) have a standard normal distribution, with mean \(0\) and variance \(1\), then \((Z+\mu)^2\) has a noncentral chi-squared distribution with one degree of freedom. The moment-generating function of \((Z+\mu)^2\) then is \[\begin{align} M(t)&=\mathbb E[e^{tX}]\\ &=\mathbb E[e^{t(Z+\mu)^2}]\\ &=\int_{-\infty}^{+\infty}\frac{1}{\sqrt{2\pi}}e^{t(z+\mu)^2}e^{-z^2/2}dz\\ &=\int_{-\infty}^{+\infty}\frac{1}{\sqrt{2\pi}}\exp(tz^2+2t\mu z-z^2/2+t\mu^2)dz\\ &=\int_{-\infty}^{+\infty}\frac{1}{\sqrt{2\pi}}\exp\left(-(\frac{1}{2}-t)z^2+2t\mu z-z^2/2+t\mu^2\right)dz\\ &=\int_{-\infty}^{+\infty}\frac{1}{\sqrt{2\pi}}\exp\left(-(\frac{1}{2}-t)(z-\frac{2\mu t}{1-2t})^2+t\mu^2+\frac{2\mu^2 t^2}{1-2t}\right)dz\\ &=\exp\left(t\mu^2+\frac{2\mu^2 t^2}{1-2t}\right)\int_{-\infty}^{+\infty}\frac{1}{\sqrt{2\pi}}\exp\left(-(\frac{1}{2}-t)(z-\frac{2\mu t}{1-2t})^2\right)dz\\ &=\exp\left(t\mu^2+\frac{2\mu^2 t^2}{1-2t}\right)\int_{-\infty}^{+\infty}\frac{1}{\sqrt{2\pi}}\exp\left(-\frac{1}{2}\frac{(z-\frac{2\mu t}{1-2t})^2}{(1-2t)^{-1}}\right)dz\\ &=\exp\left(t\mu^2+\frac{2\mu^2 t^2}{1-2t}\right)(1-2t)^{-1/2}\\ &=\exp\left(\frac{t\mu^2}{1-2t}\right)(1-2t)^{-1/2}\\ \end{align}\]

A noncentral chi-squared distributed random variable \(\chi^2_{k,\lambda}\) with \(k\) df and parameter \[\lambda=\sum_{i=1}^{k}\mu^2_i\] \(\lambda\) is sometimes called the noncentrality parameter. A noncentral chi-squared distributed random variable is the sum of the squares of \(k\) independent normal variables \(X_i=Z_i+\mu_i,\quad i=1,\cdots,k.\) That is, \[\chi^2_{k,\lambda}=\sum_{i=1}^{k}X_i^2=\sum_{i=1}^{k}(Z_i+\mu_i)^2\] This distribution arises in multivariate statistics as a derivative of the multivariate normal distribution. While the central chi-squared distribution is the squared norm of a random vector with \(N(\mathbf 0_{k},\mathbf I_{k})\) distribution (i.e., the squared distance from the origin to a point taken at random from that distribution), the non-central \(\chi^{2}\) is the squared norm of a random vector with \(N(\boldsymbol\mu,\mathbf I_{k})\) distribution. Here \(\mathbf 0_{k}\) is a zero vector of length \(k\), \(\boldsymbol\mu =(\mu_{1},\ldots ,\mu_{k})\) and \(\mathbf I_{k}\) is the identity matrix of size \(k\). The probability density function (pdf) is given by

\[f_{X}(x;k,\lambda)=\sum_{i=0}^{\infty}\frac {e^{-\lambda /2}(\lambda /2)^{i}}{i!}f_{Y_{k+2i}}(x),\] where \(Y_{q}\) is distributed as chi-squared with \(q\) degrees of freedom. From this representation, the noncentral chi-squared distribution is seen to be a Poisson-weighted mixture of central chi-squared distributions. Suppose that a random variable \(J\) has a Poisson distribution with mean \(\lambda/2\), and the conditional distribution of \(Z\) given \(J = i\) is chi-squared with \(k + 2i\) degrees of freedom. Then the unconditional distribution of \(Z\) is non-central chi-squared with \(k\) degrees of freedom, and non-centrality parameter \(\lambda\).

Because all terms are jointly independent and using the above result, we have \[\begin{align} M(t)&=\mathbb E[e^{t\chi^2_{k,\lambda}}]\\ &=\mathbb E[e^{t\sum_{i=1}^{k}(Z_i+\mu_i)^2}]\\ &=\mathbb E\left[\prod_{i}\exp\left[t(Z_i+\mu_i)^2\right]\right]\\ &=\prod_{i}\mathbb E\left[\exp\left[t(Z_i+\mu_i)^2\right]\right]\\ &=\prod_{i}\exp\left(\frac{t\mu_i^2}{1-2t}\right)(1-2t)^{-1/2}\\ &=\exp\left(\frac{t\sum_i\mu_i^2}{1-2t}\right)(1-2t)^{-k/2}\\ &=\exp\left(\frac{t\lambda}{1-2t}\right)(1-2t)^{-k/2} \quad (2t<1)\\ \end{align}\] ref

Logistic When the location parameter \(\mu\) is \(0\) and the scale parameter \(s\) is \(1\), then the probability density function of the logistic distribution is given by \[ \begin{align} f(x;0,1)&=\frac{e^{-x}}{(1+e^{-x})^2}\\ &=\frac{1}{(e^{x/2}+e^{-x/2})^2}\\ &=\frac{1}{4}\text{sech}^{2}\left(\frac{x}{2}\right). \end{align}\]

The mgf is \[ \begin{align} M(t)&=\mathbb E[e^{tx}]\\ &=\int_{-\infty}^{\infty}e^{tx}\frac{e^{-x}}{(1+e^{-x})^2}dx\\ &=\int_{1}^{0}-\left(\frac{1}{u}-1\right)^t du\quad u=\frac{1}{1+e^x}\quad du=-\frac{e^x}{(1+e^x)^2}\\ &=\int_{0}^{1}\left(\frac{1}{u}-1\right)^t du\\ &=\int_{0}^{1}u^{-t}\left(1-u\right)^t du\\ &=B(1-t, 1+t)\\ \end{align}\]

Thus in general the density is:

\[\begin{align} f(x;\mu,s)&=\frac{e^{-(x-\mu)/s}}{s\left(1+e^{-(x-\mu )/s}\right)^2}\\ &=\frac{1}{s\left(e^{(x-\mu)/(2s)}+e^{-(x-\mu )/(2s)}\right)^2}\\ &=\frac{1}{4s}\text{sech}^{2}\left(\frac {x-\mu}{2s}\right). \end{align}\]

The mgf is \[ \begin{align} M(t)&=\mathbb E[e^{tx}]\\ &=\int_{-\infty}^{\infty}e^{tx}\frac{e^{(x-\mu)/s}}{s\left(e^{(x-\mu)/s}+1\right)^2}dx\\ &=\int_{1}^{0}-\left(\frac{1}{u}-1\right)^{st}e^{\mu t} du\quad u=\frac{1}{1+e^{(x-\mu)/s}}\quad du=-\frac{e^{(x-\mu)/s}}{s\left(e^{(x-\mu)/s}+1\right)^2}\\ &=\int_{0}^{1}\left(\frac{1}{u}-1\right)^{st} e^{\mu t}du\\ &=e^{\mu t}\int_{0}^{1}u^{-st}\left(1-u\right)^{st} du\\ &=e^{\mu t}B(1-st, 1+st)\\ \end{align}\]

4.7 Exercises

Exercise 4.7.1. Suppose we play a game where we start with \(c\) dollars. On each play of the game you either double your money or half your money, with equal probability. What is your expected fortune after \(n\) trials?

Solution. Let the random variables \(X_i\) be the fortune after the \(i\)-th trial, \(X_0 = c\) always taking the value \(c\). Then:

\[ \mathbb{E}[X_{i + 1} | X_i = x] = 2x \cdot \frac{1}{2} + \frac{x}{2} \cdot \frac{1}{2} = \frac{5}{4}x \]

Taking the expectation on \(X_i\) on both sides (i.e. integrating over \(F_{X_i}(x)\)),

\[ \mathbb{E}(\mathbb{E}[X_{i + 1} | X_i = x]) = \frac{5}{4} \mathbb{E}(X_i) \Longrightarrow \mathbb{E}(X_{i+1}) = \frac{5}{4} \mathbb{E}(X_i)\]

Therefore, by induction,

\[ \mathbb{E}(X_n) = \left(\frac{5}{4}\right)^n c \]

Note that this is not a martingale, as in the traditional double-or-nothing formulation – the expected value goes up at each iteration.

Exercise 4.7.2. Show that \(\mathbb{V}(X) = 0\) if and only if there is a constant \(c\) such that \(\mathbb{P}(X = c) = 1\).

Solution. We have \(\mathbb{V}(X) = \mathbb{E}[(X - \mathbb{E}(X))^2]\):

\[ \mathbb{V}(X) = \int (x - \mu_X)^2 dF_X(x) \]

Since \((x - \mu_X)^2 \geq 0\), in order for the variance to be 0 we must have the integrand be zero with probability 1, i.e. \(\mathbb{P}(X = \mu_X) = 1\).

Exercise 4.7.3. Let \(X_1, \dots, X_n \sim \text{Uniform}(0, 1)\) and let \(Y_n = \max \{ X_1, \dots, X_n \}\). Find \(\mathbb{E}(Y_n)\).

Solution. The CDF of \(Y_n\), for \(0 \leq y \leq 1\), is:

\[ F_{Y_n}(y) = \mathbb{P}(Y_n \leq y) = \prod_{i=1}^n \mathbb{P}(X_i \leq y) = y^n \]

so its PDF is \(f_{Y_n}(y) = F'_{Y_n}(y) = n y^{n-1}\) for \(0 \leq y \leq 1\).

The expected value of \(Y_n\) then is

\[ \mathbb{E}(Y_n) = \int_0^1 y f_{Y_n}(y) dy = \int_0^1 n y^n dy = \frac{n}{n+1} \]

Exercise 4.7.4. A particle starts at the origin of the real line and moves along the line in jumps of one unit. For each jump the probability is \(p\) that the particle will move one unit to the left and the probability is \(1 - p\) that the particle will jump one unit to the right. Let \(X_n\) be the position of the particle after \(n\) units. Find \(\mathbb{E}(X_n)\) and \(\mathbb{V}(X_n)\). (This is known as a random walk.)

Solution.

We can define \(X_n = \sum_{i=1}^n (1 - 2Y_i)\), where \(Y_i \sim \text{Bernoulli}(p)\) and the \(Y_i\)’s are independent random variables representing the direction of each jump.

We then have:

\[ \mathbb{E}(X_n) = \sum_{i=1}^n \mathbb{E}(1 - 2Y_i) = \sum_{i=1}^n (1 - 2p) = n(1 - 2p) \]

and

\[ \mathbb{V}(X_n) = \sum_{i=1}^n \mathbb{V}(1 - 2Y_i) \sum_{i=1}^n 4\mathbb{V}(Y_i) = 4np(1 - p) \]

Exercise 4.7.5. A fair coin is tossed until a head is obtained. What is the expected number of tosses that will be required?

Solution. The number of tosses follows a geometric distribution, \(X \sim \text{Geom}(p)\), where \(p\) is the probability of heads. Let’s deduce its expected value, rather than use it as a known fact (\(\mathbb{E}(X) = 1/p\)). The PDF is

\[ f_X(k) = p (1 - p)^{k - 1}, \quad k = 1,2,3,\cdots \]

The expected value for \(X\) is

\[ \begin{align} \mathbb{E}(X) &= \sum_{k=1}^\infty k p (1 - p)^{k - 1} \\ &= \sum_{k=1}^\infty p(1-p)^{k-1} + \sum_{k=2}^\infty (k - 1) p(1-p)^{k - 1} \\ &= p \left( 1 + (1 - p) + (1 - p)^2 + \dots \right) + \sum_{k=1}^\infty k p(1-p)^k \\ &= p \left(\frac{1}{1 - (1 - p)}\right) + (1 - p) \sum_{k=1}^\infty k p(1-p)^{k - 1} \\ &= 1 + (1 - p) \mathbb{E}(X) \end{align} \]

from where we get \(\mathbb{E}(X) = 1 / p\).

If \[ f_X(k) = p (1 - p)^k, \quad k = 0, 1,2,3,\cdots \]

\[ \begin{align} \mathbb{E}(X) &= \sum_{k=0}^\infty k p (1 - p)^{k} \\ &= \sum_{k=1}^\infty kp(1-p)^{k}\\ &= \sum_{k=1}^\infty (k-1)p(1-p)^{k}+\sum_{k=1}^\infty p(1-p)^{k}\\ &= (1-p)\sum_{k=1}^\infty (k-1)p(1-p)^{k-1}+\sum_{k=1}^\infty p(1-p)^{k}\\ &= (1 - p)\mathbb{E}(X) +\sum_{k=1}^\infty p(1-p)^{k} \\ &= (1 - p)\mathbb{E}(X) +\sum_{k=0}^\infty p(1-p)^{k}-p \\ &= (1 - p)\mathbb{E}(X) +1-p \\ \end{align} \]

from where we get \[\mathbb{E}(X) = (1-p)/p\].

Exercise 4.7.6. Prove Theorem 4.6 for discrete random variables.

Let \(Y = r(X)\). Then

\[ \mathbb{E}(Y) = \mathbb{E}(r(X)) = \int r(x) \; dF_X(x) \]

Solution. The result is immediate from the definition of expectation:

\[ Y(\omega) = r(X(\omega)) = r(x) \quad \forall \omega : X(\omega) = x \]

and so

\[ \mathbb{E}(Y) = \int r(x) dF_x(x) \]

Exercise 4.7.7. Let \(X\) be a continuous random variable with CDF \(F\). Suppose that \(\mathbb{P}(X > 0) = 1\) and that \(\mathbb{E}(X)\) exists. Show that \(\mathbb{E}(X) = \int_0^\infty \mathbb{P}(X > x) dx\).

Hint: Consider integrating by parts. The following fact is helpful: if \(\mathbb{E}(X)\) exists then \(\lim_{x \rightarrow +\infty} x | 1 - F(x) | = 0\).

Solution. Let’s prove the following, slightly more general, lemma.

Lemma: For every continuous random variable \(X\),

\[ \mathbb{E}(X) = \int_0^\infty (1 - F_X(y)) dy - \int_{-\infty}^0 F_X(y) dy \]

Proof:

\[ \begin{align} \mathbb{E}(X) &= \int_{-\infty}^\infty x f_X(x) dx \\ &= \int_{-\infty}^0 \int_x^0 -f_X(x) dy dx + \int_0^\infty \int_0^x f_X(x) dy dx \\ &= -\int_{-\infty}^0 \int_{-\infty}^y f_X(x) dx dy + \int_0^\infty \int_y^\infty f_X(x) dx dy \\ &= -\int_{\infty}^0 \mathbb{P}(X \leq y) dy + \int_0^\infty \mathbb{P}(X \geq y) dy \\ &= \int_0^\infty (1 - F_X(y)) dy - \int_{-\infty}^0 F_X(y) dy \end{align} \]

The result follows by imposing \(\mathbb{P}(X > 0) = 1\), which implies \(\int_{-\infty}^0 F_X(y) dy = 0\).

Exercise 4.7.8. Prove Theorem 4.16.

Let \(X_1, \dots, X_n\) be IID and let \(\mu = \mathbb{E}(X_i)\), \(\sigma^2 = \mathbb{V}(X_i)\). Then

\[ \mathbb{E}\left(\overline{X}_n\right) = \mu, \quad \mathbb{V}\left(\overline{X}_n\right) = \frac{\sigma^2}{n}, \quad \text{and} \quad \mathbb{E}\left(S_n^2\right) = \sigma^2 \]

Solution.

For the expected value of sample mean:

\[ \mathbb{E}\left(\overline{X}_n\right) = \mathbb{E}\left( \frac{1}{n} \sum_{i=1}^n X_i \right) = \frac{1}{n} \sum_{i=1}^n \mathbb{E}(X_i) = \frac{1}{n} n\mu = \mu \]

For the variance of sample mean:

\[ \mathbb{V}\left(\overline{X}_n\right) = \mathbb{V}\left( \frac{1}{n} \sum_{i=1}^n X_i \right) = \frac{1}{n^2} \sum_{i=1}^n \mathbb{V}(X_i) = \frac{1}{n^2} n \sigma^2 = \frac{\sigma^2}{n} \]

For the expected value of sample variance:

\[ \begin{align} \mathbb{E}(S_n^2) &= \mathbb{E}\left(\frac{1}{n - 1} \sum_{i=1}^n \left(X_i - \overline{X}_n\right)^2 \right) \\ &= \frac{1}{n - 1} \mathbb{E} \left( \sum_{i=1}^n \left(X_i - \overline{X}_n\right)^2 \right) \\ &= \frac{1}{n - 1} \mathbb{E} \left( \sum_{i=1}^n \left(X_i^2 - 2 X_i \overline{X}_n + \overline{X}_n^2\right) \right) \\ &= \frac{1}{n - 1} \mathbb{E} \left( \sum_{i=1}^n X_i^2 - 2 \overline{X}_n \sum_{i=1}^n X_i + n \overline{X}_n^2 \right) \\ &= \frac{1}{n - 1} \mathbb{E} \left( \sum_{i=1}^n X_i^2 - 2 \overline{X}_n \cdot n \overline{X}_n + n \overline{X}_n^2 \right) \\ &= \frac{1}{n - 1} \mathbb{E} \left( \sum_{i=1}^n X_i^2 - n \overline{X}_n^2 \right) \\ &= \frac{1}{n - 1} \left( \sum_{i=1}^n \mathbb{E}(X_i^2) - n \mathbb{E}\left( \overline{X}_n^2 \right) \right) \\ &= \frac{1}{n - 1} \left( \sum_{i=1}^n \left(\mathbb{V}(X_i) + (\mathbb{E}(X_i))^2 \right) - n \left(\mathbb{V}\left( \overline{X}_n \right) + \left(\mathbb{E}\left(\overline{X}_n\right)\right)^2 \right)\right) \\ &= \frac{1}{n -1} \left( n \left( \sigma^2 + \mu^2\right) - n \left(\frac{\sigma^2}{n} + \mu^2 \right) \right) \\ &= \sigma^2 \end{align} \]

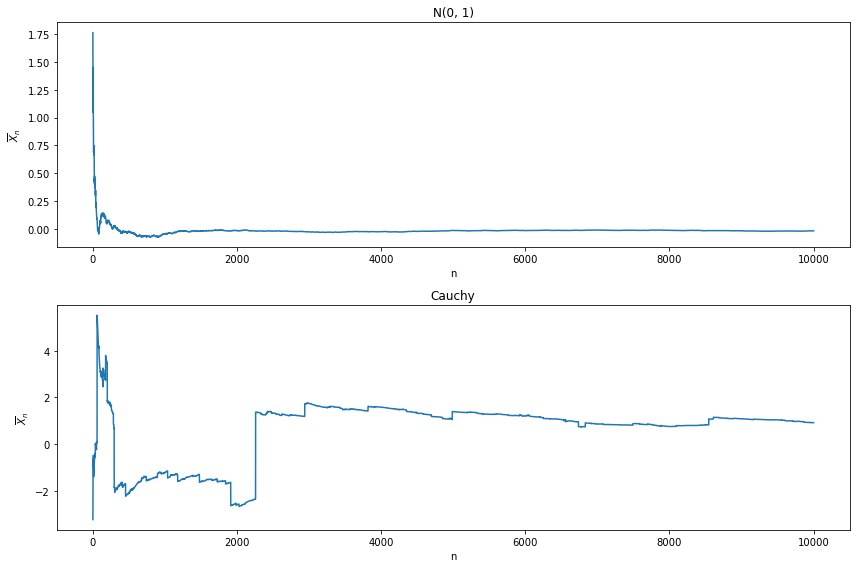

Exercise 4.7.9 (Computer Experiment). Let \(X_1, \dots, X_n\) be \(N(0, 1)\) random variables and let \(\overline{X}_n = n^{-1} \sum_{i=1}^n X_i\). Plot \(\overline{X}_n\) versus \(n\) for \(n = 1, \dots, 10,000\). Repeat for \(X_1, \dots, X_n \sim \text{Cauchy}\). Explain why there is such a difference.

import numpy as np

from scipy.stats import norm, cauchy

np.random.seed(0)

N = 10000

X = norm.rvs(size=N)

Y = cauchy.rvs(size = N)import matplotlib.pyplot as plt

%matplotlib inline

nn = np.arange(1, N + 1)

plt.figure(figsize=(12, 8))

ax = plt.subplot(2, 1, 1)

ax.plot(nn, np.cumsum(X) / nn)

ax.set_title('N(0, 1)')

ax.set_xlabel('n')

ax.set_ylabel(r'$\overline{X}_n$')

ax = plt.subplot(2, 1, 2)

ax.plot(nn, np.cumsum(Y) / nn)

ax.set_title('Cauchy')

ax.set_xlabel('n')

ax.set_ylabel(r'$\overline{X}_n$')

plt.tight_layout()

plt.show()

png

The mean on the Cauchy distribution is famously undefined: \(\overline{X}_ n\) is not going to converge.

Exercise 4.7.10. Let \(X \sim N(0, 1)\) and let \(Y = e^X\). Find \(\mathbb{E}(Y)\) and \(\mathbb{V}(Y)\).

Solution.

The CDF of \(Y\) is, for \(y > 0\):

\[ F_Y(y) = \mathbb{P}(Y \leq y) = \mathbb{P}(X \leq \log y) = \Phi(\log y) \]

and so the PDF is

\[ f_Y(y) = F'_Y(y) = \frac{d}{dy} \Phi(\log y) = \frac{d \Phi(\log y)}{d \log y} \frac{d \log y}{dy} = \frac{\phi(\log y)}{y}\]

The expected value is

\[ \mathbb{E}(Y) = \int y f_Y(y) dy = \int_0^\infty y \frac{\phi(\log y)}{y} dy = \int_0^\infty \phi(\log y)\; dy = \sqrt{e}\]

The expected value of \(Y^2\) is

\[ \mathbb{E}(Y^2) = \int y^2 f_Y(y) dy = \int_0^\infty y^2 \frac{\phi(\log y)}{y} dy = \int_0^\infty y \phi(\log y)\; dy = e^2\]

and so the variance is

\[ \mathbb{V}(Y) = \mathbb{E}(Y^2) - \mathbb{E}(Y)^2 = e(e - 1) \]

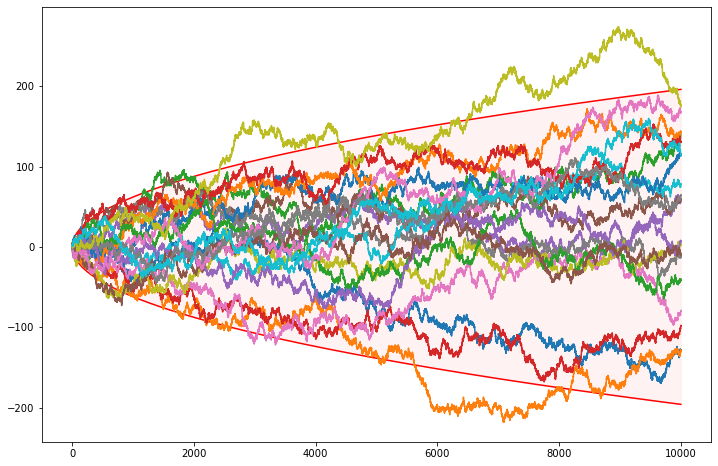

Exercise 4.7.11 (Computer Experiment: Simulating the Stock Market). Let \(Y_1, Y_2, \dots\) be independent random variables such that \(\mathbb{P}(Y_i = 1) = \mathbb{P}(Y_i = -1) = 1/2\). Let \(X_n = \sum_{i=1}^n Y_i\). Think of \(Y_i = 1\) as “the stock price increased by one dollar” \(Y_i = -1\) as “the stock price decreased by one dollar” and \(X_n\) as the value of the stock on day \(n\).

(a) Find \(\mathbb{E}(X_n)\) and \(\mathbb{V}(X_n)\).

(b) Simulate \(X_n\) and plot \(X_n\) versus \(n\) for \(n = 1, 2, \dots, 10,000\). Repeat the whole simulation several times. Notice two things. First, it’s easy to “see” patterns in the sequence even though it is random. Second, you will find that the runs look very different even though they were generated the same way. How do the calculations in (a) explain the second observation?

Solution.

(a) We have:

\[ \mathbb{E}(X_n) = \mathbb{E}\left( \sum_{i=1}^n Y_i \right) = \sum_{i=1}^n \mathbb{E}(Y_i) = 0 \]

and

\[ \begin{align} \mathbb{E}(X_n^2) &= \mathbb{E}\left( \left( \sum_{i=1}^n Y_i \right)^2 \right) \\ &= \mathbb{E}\left( \sum_{i=1}^n Y_i^2 + \sum_{i=1}^n \sum_{j = 1, j \neq i}^n Y_i Y_j \right) \\ &= \sum_{i=1}^n \mathbb{E}(Y_i^2) + \sum_{i=1}^n \sum_{j = 1, j \neq i}^n \mathbb{E}(Y_i Y_j) \\ &= \sum_{i=1}^n 1 + \sum_{i=1}^n \sum_{j = 1, j \neq i}^n 0 \\ &= n \end{align} \]

so

\[\mathbb{V}(X_n) = \mathbb{E}(X_n^2) - \mathbb{E}(X_n)^2 = n\]

(b)

import numpy as np

from scipy.stats import norm, bernoulli

N = 10000

B = 20

Y = 2 * bernoulli.rvs(p=1/2, loc=0, size=(B, N), random_state=0) - 1

X = np.cumsum(Y, axis=1)import matplotlib.pyplot as plt

%matplotlib inline

plt.figure(figsize=(12, 8))

nn = np.arange(1, N + 1)

z = norm.ppf(0.975)

plt.plot(nn, z * np.sqrt(nn), color='red')

plt.plot(nn, -z * np.sqrt(nn), color='red')

plt.fill_between(nn, z * np.sqrt(nn), -z * np.sqrt(nn), color='red', alpha=0.05)

for b in range(B):

plt.plot(nn, X[b])

plt.show()

png

The standard deviation is \(\sqrt{n}\) – it scales up with the square root of the “time”. The plot above draws \(z_{\alpha / 2} \sqrt{n}\) curves – confidence bands for \(1 - \alpha = 95\%\) – that contain most of the randomly generated path.

Exercise 4.7.12. Prove the formulas given in the table at the beginning of Section 4.4 for the Bernoulli, Poisson, Uniform, Exponential, Gamma, and Beta. Here are some hints. For the mean of the Poisson, use the fact that \(e^a = \sum_{x=0}^a a^x / x!\). To compute the variance, first compute \(\mathbb{E}(X(X - 1))\). For the mean of the Gamma, it will help to multiply and divide by \(\Gamma(\alpha + 1) / \beta^{\alpha + 1}\) and use the fact that a Gamma density integrates to 1. For the Beta, multiply and divide by \(\Gamma(\alpha + 1) \Gamma(\beta) / \Gamma(\alpha + \beta + 1)\).

Solution.

We will do all expressions in the table instead (other than multinomial and multivariate normal, where proofs are already provided in the book).

Point mass at \(p\)

Let \(X\) have a point mass at \(p\). Then:

- \(\mathbb{E}(X) = p \cdot 1 = p\)

- \(\mathbb{E}(X^2) = p^2 \cdot 1 = p^2\)

- \(\mathbb{V}(X) = \mathbb{E}(X^2) - \mathbb{E}(X)^2 = p^2 - p^2 = 0\)

Bernoulli

Let \(X \sim \text{Bernoulli}(p)\). Then:

- \[\mathbb{E}(X) = 1 \cdot p + 0 \cdot (1 - p) = p \]

- \[\mathbb{E}(X^2) = 1 \cdot p + 0 \cdot (1 - p) = p\]

- \[\mathbb{V}(X) = \mathbb{E}(X^2) - \mathbb{E}(X)^2 = p(1 - p)\]

Binomial

Let \(X \sim \text{Binomial}(n, p)\). Then \(X = \sum_{i=1}^n Y_i\), where \(Y_i \sim \text{Bernoulli}(p)\) are IID random variables.

- \[\mathbb{E}(X) = \mathbb{E}\left( \sum_{i=1}^n Y_i \right) = \sum_{i=1}^n \mathbb{E}(Y_i) = np \]

- \[\mathbb{V}(X) = \mathbb{V}\left(\sum_{i=1}^n Y_i \right) = \sum_{i=1}^n \mathbb{V}(Y_i) = np(1-p) \]

Geometric

Geometric distribution: \[ f_X(k) = p (1 - p)^{k-1}, \quad k = 1,2,3,\cdots \] The expectation:

\[ \begin{align} \mathbb{E}(X) &= \sum_{k=1}^\infty k p (1 - p)^{k - 1} \\ &= \sum_{k=1}^\infty p(1-p)^{k-1} + \sum_{k=2}^\infty (k - 1) p(1-p)^{k - 1} \\ &= 1 + \sum_{k=1}^\infty k p(1-p)^k \\ &= 1 + (1 - p) \sum_{k=1}^\infty k p(1-p)^{k - 1} \\ &= 1 + (1 - p) \mathbb{E}(X) \end{align} \]

Solving for the expectation, we get \(\mathbb{E}(X) = 1/p\).

Another version of Geometric distribution: \[ f_X(k) = p (1 - p)^k, \quad k = 0, 1,2,3,\cdots \]

\[ \begin{align} \mathbb{E}(X) &= \sum_{k=0}^\infty k p (1 - p)^{k} \\ &= \sum_{k=1}^\infty kp(1-p)^{k}\\ &= \sum_{k=1}^\infty (k-1)p(1-p)^{k}+\sum_{k=1}^\infty p(1-p)^{k}\\ &= (1-p)\sum_{k=1}^\infty (k-1)p(1-p)^{k-1}+\sum_{k=1}^\infty p(1-p)^{k}\\ &= (1 - p)\mathbb{E}(X) +\sum_{k=1}^\infty p(1-p)^{k} \\ &= (1 - p)\mathbb{E}(X) +\sum_{k=0}^\infty p(1-p)^{k}-p \\ &= (1 - p)\mathbb{E}(X) +1-p \\ \end{align} \]

from where we get \[\mathbb{E}(X) = (1-p)/p\]

For the variance we also have:

\[ \begin{align} \mathbb{E}(X^2) &= \sum_{k=1}^\infty k^2 p (1 - p)^{k - 1} \\ &= \sum_{k=1}^\infty k p(1-p)^{k-1} + \sum_{k=2}^\infty (k^2 - k) p(1-p)^{k - 1} \\ &= \mathbb{E}(X) + (1 - p) \sum_{k=1}^\infty (k^2 + k) p(1-p)^{k - 1} \\ &= \mathbb{E}(X) + (1 - p) \mathbb{E}(X) + (1 - p) \sum_{k=1}^\infty k^2 p(1-p)^{k-1} \\ &= \frac{2 - p}{p} + (1 - p) \mathbb{E}(X^2) \end{align} \]

Solving for the expectation, we get \(\mathbb{E}(X^2) = (2 - p) / p^2\).

Finally,

\[ \mathbb{V}(X) = \mathbb{E}(X^2) - \mathbb{E}(X)^2 = \frac{2 - p}{p^2} - \frac{1}{p^2} = \frac{1 - p}{p^2} \]

For the variant version of Geometric distribution: \[ f_X(k) = p (1 - p)^k, \quad k = 0, 1,2,3,\cdots \] \[ \begin{align} \mathbb{E}(X^2) &= \sum_{k=0}^\infty k^2 p (1 - p)^{k} \\ &= \sum_{k=1}^\infty k^2 p(1-p)^{k}\\ &= \sum_{k=0}^\infty (k+1)^2 p(1-p)^{k+1}\\ &= \sum_{k=0}^\infty k^2 p(1-p)^{k+1}+2\sum_{k=0}^\infty k p(1-p)^{k+1}+\sum_{k=0}^\infty p(1-p)^{k+1}\\ &= (1-p)\mathbb{E}(X^2)+2(1-p)\mathbb{E}(X)+(1-p)\\ &= (1-p)\mathbb{E}(X^2)+2(1-p)^2/p+(1-p)\\ &= (1-p)\mathbb{E}(X^2)+\frac{2(1-p)^2}{p}+\frac{p(1-p)}{p}\\ &= (1-p)\mathbb{E}(X^2)+\frac{2-3p+p^2}{p}\\ \end{align} \] We get \[\mathbb{E}(X^2) = \frac{2-3p+p^2}{p^2}\] And then the variance: \[ \mathbb{V}(X) = \mathbb{E}(X^2) - \mathbb{E}(X)^2 = \frac{2-3p+p^2}{p^2} - \frac{(1-p)^2}{p^2} = \frac{1 - p}{p^2} \]

Because the two distributions are linked in the following way

\[Y=X-1\]

Thus using expectation property you get that

\[E(Y)=E(X)-1\]

That is

\[E(Y)=\frac{1}{p}-1=\frac{1-p}{p}\]

But, using variance property,

\[V(Y)=V(X-1)=V(X)\]

Cauchy

Let \[f_X(x) = \frac{1}{\pi[1+(x-\theta)^2]},\quad -\infty<x<\infty\quad -\infty<\theta<\infty\]. Then: \[\mathbb{E}|X|=\int_{-\infty}^{\infty}\frac{|x|}{\pi([1+(x-\theta)^2])}dx=\frac{2}{\pi}\int_{0}^{\infty}\frac{x}{[1+(x-\theta)^2]}dx=\frac{2}{\pi}\frac{\log([1+(x-\theta)^2])}{2}\bigg|_{0}^{\infty}=\infty\] so \(\mathbb{E}X\) does not exist.

Poisson

Let \(X \sim \text{Poisson}(\lambda)\). Then:

\[ \mathbb{E}(X) = \sum_{k=0}^\infty k \frac{\lambda^k e^{-\lambda}}{k!} = \lambda e^{-\lambda} \sum_{k=1}^\infty \frac{\lambda^{k - 1} }{(k - 1)!} = \lambda e^{-\lambda} \sum_{k=0}^\infty \frac{\lambda^k}{k!} = \lambda e^{-\lambda} e^{\lambda} = \lambda \]

\[ \mathbb{E}(X^2) = \sum_{k=0}^\infty k^2 \frac{\lambda^k e^{-\lambda}}{k!} = \lambda \sum_{k=1}^\infty k \frac{\lambda^{k-1} e^{-\lambda} }{(k-1)!} = \lambda \sum_{k=0}^\infty (k + 1) \frac{\lambda^{k} e^{-\lambda} }{k!} = \lambda \mathbb{E}(X + 1) = \lambda(\lambda + 1) \]

\[ \mathbb{V}(X) = \mathbb{E}(X^2) - \mathbb{E}(X)^2 = \lambda^2 + \lambda - \lambda^2 = \lambda \]

Uniform

Let \(X \sim \text{Uniform}(a, b)\). Then:

- \[\mathbb{E}(X) = \int_a^b x \frac{1}{b - a} dx = \frac{a + b}{2}\]

- \[\mathbb{E}(X^2) = \int_a^b x^2 \frac{1}{b - a} dx = \frac{a^2 + ab + b^2}{3}\]

- \[\mathbb{V}(X) = \mathbb{E}(X^2) - \mathbb{E}(X)^2 = \frac{a^2 + ab + b^2}{3} - \frac{a^2 + 2ab + b^2}{4} = \frac{(b - a)^2}{12}\]

Normal

Let \(X \sim N(\mu, \sigma^2)\). Converting into a standard normal, we get \(Z = (X - \mu) / \sigma \sim N(0, 1)\). Then:

- \[ \mathbb{E}(X) = \mathbb{E}(\sigma Z + \mu) = \sigma \mathbb{E}(Z) + \mu = \mu\]

- \[ \mathbb{V}(X) = \mathbb{V}(\sigma Z + \mu) = \sigma^2 \mathbb{V}(Z) = \sigma^2\]

To prove that the expected value \(Z\) is 0, note that the PDF of \(Z\) is even, \(\phi(z) = \phi(-z)\), so

\[ \mathbb{E}(Z) = \int_{-\infty}^\infty z \phi(z) dz = \int_{-\infty}^0 z \phi(z) dz + \int_0^\infty z \phi(z) dz \\ = \int_0^\infty -z \phi(-z) dz + \int_0^\infty z \phi(z) dz = \int_0^\infty (-z + z)\phi(z) = 0 \]

To prove that the variance of \(Z\) is 0, write out the integral explicitly for the expectation of \(Z^2\),

\[ \mathbb{E}(Z^2) = \int_{-\infty}^\infty z^2 \phi(z) dz = \frac{1}{\sqrt{2 \pi}} \int_{-\infty}^\infty z^2 e^{-z^2/2} dz\\ = \left[ \Phi(z) - \frac{1}{\sqrt{2 \pi}} z e^{-z^2/2} \right]_{-\infty}^\infty = \lim_{x \rightarrow +\infty} \Phi(x) - \lim_{x \rightarrow -\infty} \Phi(x) = 1 - 0 = 1 \]

and so

\[\mathbb{V}(Z) = \mathbb{E}(Z^2) - \mathbb{E}(Z)^2 = 1 - 0 = 1\]

Exponential

Let \(X \sim \text{Exponential}(\beta)\). Then:

- \[ \mathbb{E}(X) = \int_0^\infty x \frac{1}{\beta} e^{-x / \beta} dx = \frac{1}{\beta} \int_0^\infty x e^{-x / \beta} dx = \frac{1}{\beta} \beta^2 = \beta\]

- \[\mathbb{E}(X^2) = \int_0^\infty x^2 \frac{1}{\beta} e^{-x / \beta} dx = \frac{1}{\beta} \int_0^\infty x^2 e^{-x / \beta} dx = \frac{1}{\beta} 2\beta^3 = 2 \beta^2 \]

- \[ \mathbb{V}(X) = \mathbb{E}(X^2) - \mathbb{E}(X)^2 = 2\beta^2 - \beta^2 = \beta^2\]

Gamma

Let \(X \sim \text{Gamma}(\alpha, \beta)\). The PDF is

\[ f_X(x) = \frac{\beta^\alpha}{\Gamma(\alpha)} x^{\alpha - 1} e^{-\beta x} \quad \text{for } x > 0 \]

We have:

\[ \begin{align} \mathbb{E}(X) &= \int x f_X(x) dx \\ &= \int_0^\infty x \frac{\beta^\alpha}{\Gamma(\alpha)} x^{\alpha - 1} e^{-\beta x} dx \\ &= \frac{\alpha}{\beta} \int_0^\infty\frac{\beta^{\alpha + 1}}{\Gamma(\alpha + 1)} x^\alpha e^{-\beta x} dx \\ &= \frac{\alpha}{\beta} \end{align} \]

where we used that

- \(\alpha \Gamma(\alpha) = \Gamma(\alpha + 1)\),

- and last integral is the PDF of \(\text{Gamma}(\alpha + 1, \beta)\), integrated over its entire domain.

We also have:

\[ \begin{align} \mathbb{E}(X^2) &= \int x^2 f_X(x) dx \\ &= \int_0^\infty x^2 \frac{\beta^\alpha}{\Gamma(\alpha)} x^{\alpha - 1} e^{-\beta x} dx \\ &= \frac{\alpha (\alpha + 1)}{\beta^2} \int_0^\infty\frac{\beta^{\alpha + 2}}{\Gamma(\alpha + 2)} x^{\alpha + 1} e^{-\beta x} dx \\ &= \frac{\alpha (\alpha + 1)}{\beta^2} \end{align} \]

- \(\alpha(\alpha + 1) \Gamma(\alpha) = \Gamma(\alpha + 2)\),

- and last integral is the PDF of \(\text{Gamma}(\alpha + 2, \beta)\), integrated over its entire domain.

Therefore,

\[ \mathbb{V}(X) = \mathbb{E}(X^2) - \mathbb{E}(X)^2 = \frac{\alpha (\alpha + 1)}{\beta^2} - \frac{\alpha^2}{\beta^2} = \frac{\alpha}{\beta^2} \]

Beta

Let \(X \sim \text{Beta}(\alpha, \beta)\). The PDF is

\[f_X(x) = \frac{\Gamma(\alpha + \beta)}{\Gamma(\alpha) \Gamma(\beta)} x^{\alpha - 1}(1 - x)^{\beta - 1} \quad \text{for } x > 0\]

We have:

\[ \begin{align} \mathbb{E}(X) &= \int x f_X(x) dx \\ &= \int_0^\infty x \frac{\Gamma(\alpha + \beta)}{\Gamma(\alpha) \Gamma(\beta)} x^{\alpha - 1}(1 - x)^{\beta - 1} dx \\ &= \frac{\alpha}{\alpha + \beta} \int_0^\infty \frac{\Gamma(\alpha + \beta + 1)}{\Gamma(\alpha + 1) \Gamma(\beta)} x^{\alpha}(1 - x)^{\beta - 1} dx \\ &= \frac{\alpha}{\alpha + \beta} \end{align} \]

where we used that

- \(\alpha \Gamma(\alpha) = \Gamma(\alpha + 1)\),

- \((\alpha + \beta) \Gamma(\alpha + \beta) = \Gamma(\alpha + \beta + 1)\),

- and the last integral is the PDF of \(\text{Beta}(\alpha + 1, \beta)\), integrated over its entire domain.

We also have:

\[ \begin{align} \mathbb{E}(X^2) &= \int x^2 f_X(x) dx \\ &= \int_0^\infty x^2 \frac{\Gamma(\alpha + \beta)}{\Gamma(\alpha) \Gamma(\beta)} x^{\alpha - 1}(1 - x)^{\beta - 1} dx \\ &= \frac{\alpha (\alpha + 1)}{(\alpha + \beta)(\alpha + \beta + 1)} \int_0^\infty \frac{\Gamma(\alpha + \beta + 2)}{\Gamma(\alpha + 2) \Gamma(\beta)} x^{\alpha + 1}(1 - x)^{\beta - 1} dx \\ &= \frac{\alpha (\alpha + 1)}{(\alpha + \beta)(\alpha + \beta + 1)} \end{align} \]

where we used that

- \(\alpha (\alpha + 1) \Gamma(\alpha) = \Gamma(\alpha + 2)\),

- \((\alpha + \beta) (\alpha + \beta + 1) \Gamma(\alpha + \beta) = \Gamma(\alpha + \beta + 2)\),

- and the last integral is the PDF of \(\text{Beta}(\alpha + 2, \beta)\), integrated over its entire domain.

Therefore,

\[ \mathbb{V}(X) = \mathbb{E}(X^2) - \mathbb{E}(X)^2 = \frac{\alpha (\alpha + 1)}{(\alpha + \beta)(\alpha + \beta + 1)} - \frac{\alpha^2}{(\alpha + \beta)^2} = \frac{\alpha \beta}{(\alpha + \beta)^2 (\alpha + \beta + 1)} \]

\(t\)-student

Let \(X_1,\cdots,X_n\) be a random sample from a \(\text{n}(\mu, \sigma^2)\) distribution. The quantity \[\frac{(\bar{X}-\mu)}{(\sigma/\sqrt{n})}\] has a standard normal distribution (i.e. normal with expected mean 0 and variance 1). The quantity \[\frac{(\bar{X}-\mu)}{(S/\sqrt{n})}\] has Student’s \(t\) distribution with \(p\) degrees of freedom. And \[\frac{(\bar{X}-\mu)}{(S/\sqrt{n})}=\frac{(\bar{X}-\mu)/(\sigma/\sqrt{n})}{\sqrt{S^2/\sigma^2}}=\frac{U}{\sqrt{V/p}}\], the numerator \(U\) is a \(n(0,1)\) random variable, and the denominator \(\sqrt{V/p}\) is \(\sqrt{\chi_{n-1}^2/(n-1)}\) independent of the numerator.

Since the joint pdf of \(U\) and \(V\) is \[f_{U,V}(u,v)=\frac{1}{\sqrt{2\pi}}e^{-u^2/2}\frac{1}{\Gamma(\frac{p}{2})2^{p/2}}v^{p/2-1}e^{-v/2} \quad -\infty<u,v<+\infty\] Now make the transformation, \[t=\frac{u}{\sqrt{v/p}}, \quad w=v\] The Jacobian of the transformation is \[J=\begin{vmatrix}\frac{\partial u}{\partial t} &\frac{\partial u}{\partial w}\\ \frac{\partial v}{\partial t} & \frac{\partial v}{\partial w} \end{vmatrix}=\begin{vmatrix}(w/p)^{1/2} &0 \\ 0 & 1 \end{vmatrix}=(w/p)^{1/2}\], and the marginal pdf of

\[\begin{align} f_{T}(t)&=\int_{0}^{\infty}f_{U,V}\left(t\left(\frac{w}{p}\right)^{1/2},w\right)\left(\frac{w}{p}\right)^{1/2}dw\\ &=\frac{1}{\sqrt{2\pi}}\frac{1}{\Gamma(\frac{p}{2})2^{p/2}}\int_{0}^{\infty}e^{-(1/2)t^2 w/p}w^{p/2-1}e^{-w/2}\left(\frac{w}{p}\right)^{1/2}dw\\ &=\frac{1}{\sqrt{2\pi}}\frac{1}{\Gamma(\frac{p}{2})2^{p/2}p^{1/2}}\int_{0}^{\infty}e^{-(1/2)t^2 w/p}w^{p/2-1}e^{-w/2}w^{1/2}dw\\ &=\frac{1}{\sqrt{2\pi}}\frac{1}{\Gamma(\frac{p}{2})2^{p/2}p^{1/2}}\int_{0}^{\infty}w^{((p+1)/2)-1} e^{-(1/2)(1+t^2/p)w}dw\\ \end{align}\] Recognize the integrand as the kernel of a \(gamma\left(\frac{p+1}{2},\frac{2}{1+t^2/p}\right)\) pdf. We therefore have \[\begin{align} f_{T}(t)&=\frac{1}{\sqrt{2\pi}}\frac{1}{\Gamma(\frac{p}{2})2^{p/2}p^{1/2}}\Gamma\left(\frac{p+1}{2}\right)\left[\frac{2}{1+t^2/p}\right]^{(p+1)/2}\\ &=\frac{1}{\sqrt{p\pi}}\frac{1}{\Gamma(\frac{p}{2})}\Gamma\left(\frac{p+1}{2}\right)\left[\frac{1}{1+t^2/p}\right]^{(p+1)/2}\\ \end{align}\]

Let \(X \sim t_p\). The PDF for the t-student distribution is

\[ f_X(x) = \frac{1}{\sqrt{p \pi}} \frac{\Gamma\left(\frac{p + 1}{2}\right)}{\Gamma\left(\frac{p}{2}\right)} \frac{1}{\left(1 + \frac{x^2}{p} \right)^{(p + 1)/2}} \]

Since the PDF is even, \(f_X(x) = f_X(-x)\), the expectation will be \(0\) when it is defined:

\[ \mathbb{E}(X) = \int_{-\infty}^\infty x f_X(x) dx = \int_{-\infty}^0 x f_X(x) dx + \int_0^\infty x f_X(x) dx \\ = \int_0^\infty -x f_X(-x) dx + \int_0^\infty x f_X(x) dx = \int_0^\infty (-x + x)f_X(x) dx = 0 \]

But

\[ \mathbb{E}(X) = \int_{-\infty}^\infty x f_X(x) dx = \frac{1}{\sqrt{p \pi}} \frac{\Gamma\left(\frac{p + 1}{2}\right)}{\Gamma\left(\frac{p}{2}\right)} \int_{-\infty}^\infty x \left(1 + \frac{x^2}{p} \right)^{-(p + 1)/2} dx \]

For the expectation of \(X^2\), assuming it is defined, we have:

\[ \begin{align} \mathbb{E}(X^2) &= \int_{-\infty}^\infty x^2 f_X(x) dx \\ &= \frac{1}{\sqrt{p \pi}} \frac{\Gamma\left(\frac{p + 1}{2}\right)}{\Gamma\left(\frac{p}{2}\right)} \int_{-\infty}^\infty x^2 \left( 1 + \frac{x^2}{p}\right)^{-(p + 1) / 2} dx \\ &= \frac{p}{\sqrt{\pi}} \frac{\Gamma\left(\frac{p + 1}{2}\right)}{\Gamma\left(\frac{p}{2}\right)} \int_0^1 y^{p /2 - 2} \left( 1 - y \right)^{1 / 2} dy \\ &= \frac{p}{\sqrt{\pi}} \frac{\Gamma\left(\frac{p + 1}{2}\right)}{\Gamma\left(\frac{p}{2}\right)} \frac{\Gamma\left(\frac{p}{2} - 1\right) \Gamma\left(\frac{3}{2}\right)}{\Gamma\left(\frac{p + 1}{2}\right)} \\ &= \frac{p}{p - 2} \end{align} \]

where we used:

- A variable replacement \(y = \left( 1 + \frac{x^2}{p} \right)^{-1}\)

- The property that \(\int_0^1 y^{p - 1} (1 - y)^{q - 1} dy = \frac{\Gamma(p) \Gamma(q)}{\Gamma(p + q)}\), since this is the integral of the PDF of \(\Gamma(p, q)\) scaled by a factor of \(\frac{\Gamma(p) \Gamma(q)}{\Gamma(p + q)}\), with \(p = p / 2 - 1, \quad p>2\), \(q = 3/2\)

- \(\Gamma(3 / 2) = \sqrt{\pi}/2\)

Finally,

\[ \mathbb{V}(X) = \mathbb{E}(X^2) - \mathbb{E}(X)^2 = \frac{p}{p - 2} \]

Reference: https://math.stackexchange.com/a/1502519

\(\chi^2\) distribution

Let \(X \sim \chi^2_k\). Then \(X\) has the same distributions as the sum of squares of \(k\) IID standard Normal random variables, \(X = \sum_{i=1}^k Z_i^2\), \(Z_i \sim N(0, 1)\).

Chi-squared distribution PDF: \[ f_X(x) = \frac{1}{2^{p/2}\Gamma(p/2)} x^{(p/2) - 1} e^{- x/2}=Gamma(p/2,1/2) \quad \text{for } x > 0 \]

The expectation of \(X\) can then be computed:

\[ \mathbb{E}(X) = \mathbb{E}\left( \sum_{i=1}^k Z_i^2 \right) = \sum_{i=1}^k \mathbb{E}(Z_i^2) = \sum_{i=1}^k (\mathbb{V}(Z_i) + \mathbb{E}(Z_i)^2) = \sum_{i=1}^k (1 + 0) = k \]

The expectation of \(X^2\) is:

\[ \begin{align} \mathbb{E}(X^2) &= \mathbb{E}\left( \left( \sum_{i=1}^k Z_i^2 \right)^2 \right) \\ &= \mathbb{E}\left( \sum_{i=1}^k Z_i^4 + \sum_{i=1}^k \sum_{j=1; j \neq i}^k Z_i^2 Z_j^2 \right) \\ &= \sum_{i=1}^k \mathbb{E}(Z_i^4) + \sum_{i=1}^k \sum_{j=1; j \neq i}^k \mathbb{E}(Z_i^2) \mathbb{E}(Z_j^2) \end{align} \]

But we have:

\[ \mathbb{E}(Z_i^2) = \mathbb{V}(Z_i) + \mathbb{E}(Z_i)^2 = 1 + 0 = 1 \]

and, using moment generating functions,

\[M_Z(t) = e^{t^2 / 2}\]

and taking the fourth derivative,

\[ M_Z^{(4)}(t) = 3 M_Z^{(2)}(t) + t M_Z^{(3)}(t)\]

Setting \(t = 0\) gives us \(\mathbb{E}(Z_i^4) = 3\).

Replacing it back on the expectation expression for \(X^2\),

\[ \mathbb{E}(X^2) = \sum_{i=1}^k 3 + \sum_{i=1}^k \sum_{j=1; j \neq i}^k 1 \cdot 1 = 3k + k(k-1) = k^2 + 2k \]

Therefore,

\[ \mathbb{V}(X) = \mathbb{E}(X^2) - \mathbb{E}(X)^2 = k^2 + 2k - k^2 = 2k \]

The proofs for the multinomial and mutivariate normal distribution expressions are provided in the book text (and there are notes above).

noncentral \(\chi^2\) distribution

Let \(X \sim \chi^2_k\) with \(p\) degrees of freedom and noncentrality parameter \(\lambda\). Then \(X\) has the same distributions as a mixture distribution, made up of central chi squared densities and Poisson distributions. That is we set up the hierarchy

\[\begin{align}

X|K&\sim \chi_{p+2K}^2\\

K&\sim Poisson(\lambda)

\end{align}\]

The noncentral Chi-squared distribution PDF: \[ f(x|\lambda,p) = \sum_{k=0}^{\infty}\frac{x^{p/2+k-1}e^{-x/2}}{\Gamma(p/2+k)2^{p/2+k}}\frac{\lambda^ke^{-\lambda}}{k!} =\sum_{k=0}^{\infty}Gamma(\frac{p}{2}+k, \frac{1}{2})Poisson(\lambda)\]

The marginal distribution of \(X\) is given by \[\begin{align} \mathbb E{X}&=\mathbb E(\mathbb E(X|K))\\ &=\mathbb E(p+2K)\\ &=p+2\lambda\\ \end{align}\]

Inverse \(\chi^2\) distribution

The inverse-chi-squared distribution (or inverted-chi-square distribution) is the probability distribution of a random variable whose multiplicative inverse (reciprocal) has a chi-squared distribution. It is also often defined as the distribution of a random variable whose reciprocal divided by its degrees of freedom is a chi-squared distribution. That is, if \(X\) has the chi-squared distribution with \(p\) degrees of freedom, then according to the first definition, \(1/X\) has the inverse-chi-squared distribution with \(p\) degrees of freedom; while according to the second definition, \(p/X\) has the inverse-chi-squared distribution with \(p\) degrees of freedom.

The first definition yields a probability density function given by \[f(x,p)=\frac{2^{-p/2}}{\Gamma(p/2)}x^{-p/2-1}e^{-1/(2x)}\quad 0<x<\infty\] \(p\) is the degrees of freedom parameter.

\[\begin{align}\mathbb E f(x,p)&=\frac{2^{-p/2}}{\Gamma(p/2)}\int_{0}^{\infty}x^{-p/2}e^{-1/(2x)}dx\\ &=\frac{2^{-p/2}}{\Gamma(p/2)}\int_{\infty}^{0}-y^{p/2}e^{-(1/2)y}y^{-2}dy\quad(y=1/x,\quad dy=-1/x^2 dx)\\ &=\frac{2^{-p/2}}{\Gamma(p/2)}\int_{0}^{\infty}y^{(p/2)-2}e^{-(1/2)y}dy\\ &=\frac{2^{-p/2}}{\Gamma(p/2)}\Gamma(p/2-1)2^{(p/2-1)}\\ &=\frac{1/2}{p/2-1}\\ &=\frac{1}{p-2}\quad (p>2) \end{align}\]

\(F\)-distribution

Let \(X_1,\cdots,X_n\) be a random sample from a \(n(\mu_X, \sigma_X^2)\) population, and let \(Y_1,\cdots,X_m\) be a random sample from an independent \(n(\mu_Y, \sigma_Y^2)\) population. If we were interested in comparing the variability of the populations, one quantity of interest would be the ratio \(\sigma_X^2/\sigma_Y^2\). Information about this ratio is contained in \(S_X^2/S_Y^2\), the ratio of sample variances. The \(F\) distribution allows us to compare these quantities by giving us a distribution of \[F=\frac{S_X^2/S_Y^2}{\sigma_X^2/\sigma_Y^2}=\frac{S_X^2/\sigma_X^2}{S_Y^2/\sigma_Y^2}\] with \(n-1, m-1\) degree of freedom. The ratios \(S_X^2/\sigma_X^2, S_Y^2/\sigma_Y^2\) are each scaled chi squared variates, and they are independent.

Let \(V\sim \chi^2(n)\) and \(W\sim \chi^2(m)\) independent r.v.

To find the PDF for \(X=\frac{V/n}{W/m}\).

Define \(h(v,w)=(v,v/n\cdot m/w)=(v,x)\). So, \(h^{-1}(v,x)=(v,\frac{v \cdot m}{x\cdot n})\)

Since \(f_{V,X}=f_{V,W}(h^{-1}(v,x))\cdot |det(Dh^{-1}(v,x))|\).

Because they are independent, \(f_{V,W}=f_{V}\cdot f_{W}\).

When V and U are two \(\chi^2\) independent random variables: \(f_V(v)=\frac{(\frac{1}{2})^{\frac{m}{2}}}{\Gamma(\frac{m}{2})}v^{(\frac{m}{2})-1}e^{-\frac{1}{2}v}\)

\(f_U(u)=\frac{(\frac{1}{2})^{\frac{n}{2}}}{\Gamma(\frac{n}{2})}u^{(\frac{n}{2})-1}e^{-\frac{1}{2}u}\)

with \(m\) and \(n\) degrees of freedom, then, the pdf for \(W=V/U\) is:

\[\begin{align}

f_{V/U}(\omega)&=\int_{0}^{+\infty}|u|f_U(u)f_V(u\omega)du\\

&=\int_{0}^{+\infty}u\frac{(\frac{1}{2})^{\frac{n}{2}}}{\Gamma(\frac{n}{2})}u^{\frac{n}{2}-1}e^{-\frac{1}{2}u} \frac{(\frac{1}{2})^{\frac{m}{2}}}{\Gamma(\frac{m}{2})}(u\omega)^{\frac{m}{2}-1}e^{-\frac{1}{2}u\omega}du\\

&=\frac{(\frac{1}{2})^{\frac{n}{2}}}{\Gamma(\frac{n}{2})}\frac{(\frac{1}{2})^{\frac{m}{2}}}{\Gamma(\frac{m}{2})} \omega^{\frac{m}{2}-1} \int_{0}^{+\infty}u^{\frac{n}{2}}u^{\frac{m}{2}-1} e^{-\frac{1}{2}u(1+\omega)}du\\

&=\frac{(\frac{1}{2})^{\frac{n}{2}}}{\Gamma(\frac{n}{2})}\frac{(\frac{1}{2})^{\frac{m}{2}}}{\Gamma(\frac{m}{2})} \omega^{\frac{m}{2}-1} \int_{0}^{+\infty}u^{\frac{n+m}{2}-1} e^{-\frac{1}{2}u(1+\omega)}du\\

&=\frac{(\frac{1}{2})^{\frac{n}{2}}}{\Gamma(\frac{n}{2})}\frac{(\frac{1}{2})^{\frac{m}{2}}}{\Gamma(\frac{m}{2})} \omega^{\frac{m}{2}-1} (\frac{\Gamma(\frac{n+m}{2})}{(\frac{1}{2}(1+\omega))^{\frac{n+m}{2}}})\\

&=\frac{\Gamma(\frac{n+m}{2})}{\Gamma(\frac{n}{2})\Gamma(\frac{m}{2})}\frac{\omega^{\frac{m}{2}-1}}{(1+\omega)^{\frac{n+m}{2}}}

\end{align}\]

Then, the pdf for \(W=\frac{V/m}{U/n}\) is: \[\begin{align} f_{\frac{V/m}{U/n}}&=f_{\frac{n}{m}V/U}\\ &=\frac{m}{n}f_{V/U}(\frac{m}{n}\omega)\\ &=\frac{m}{n}\frac{\Gamma(\frac{n+m}{2})}{\Gamma(\frac{n}{2})\Gamma(\frac{m}{2})}\frac{(\frac{m}{n}\omega)^{\frac{m}{2}-1}}{(1+\frac{m}{n}\omega)^{\frac{n+m}{2}}}\\ &=\frac{\Gamma(\frac{n+m}{2})}{\Gamma(\frac{n}{2})\Gamma(\frac{m}{2})}\frac{m}{n}\frac{(\frac{m}{n}\omega)^{\frac{m}{2}-1}}{(n+m\omega)^{\frac{n+m}{2}}}n^{\frac{n+m}{2}}\\ &=\frac{\Gamma(\frac{n+m}{2})}{\Gamma(\frac{n}{2})\Gamma(\frac{m}{2})}\frac{m^{\frac{m}{2}}n^{\frac{n}{2}}\omega^{\frac{m}{2}-1}}{(n+m\omega)^{\frac{n+m}{2}}} \end{align}\]

The random variable \(F\) has the \(F\) distribution with \(p\) and \(q\) degrees of freedom if it has pdf \[f_F(x)=\frac{\Gamma\left(\frac{p+q}{2}\right)}{\Gamma\left(\frac{p}{2}\right)\Gamma\left(\frac{q}{2}\right)}\left(\frac{p}{q}\right)^{p/2}\frac{x^{(p/2)-1}}{[1+(p/q)x]^{(p+q)/2}},\quad 0<x<\infty\] The \(F\) pdf is pdf of \((U/p)/(V/q)\), where \(U\) and \(V\) are independent, \(U \sim \chi_p^2\) and \(V \sim \chi_q^2\).

\[\begin{align}\mathbb E F_{n-1,m-1}&=\mathbb E\left(\frac{\chi_{n-1}^2/(n-1)}{\chi_{m-1}^2/(m-1)}\right)\\ &=\mathbb E\left(\frac{\chi_{n-1}^2}{n-1}\right)\mathbb E\left(\frac{m-1}{\chi_{m-1}^2}\right)\\ &=\left(\frac{n-1}{n-1}\right)\left(\frac{m-1}{m-3}\right)\\ &=\frac{m-1}{m-3} \end{align}\]

\(F_{\alpha,n,m}=1/F_{1−\alpha,m,n}\)

If \(X\) is Fisher distribution variable,

\[X = \frac{ \frac{A}{n} } { \frac{B}{m} }\]

where \(A\) and \(B\) follow \(\chi^2\) distributions, are independent, and have \(n\), \(m\) degrees of freedom respectively. Then the following holds:

\[\frac{1}{X} = \frac{ \frac{B}{m} } { \frac{A}{n} }\] which is also a Fisher distribution variable, and have \(m\), \(n\) degrees of freedom respectively.

Since \[ 1/F_{(m,n)} = F_{(n,m)}, \] by the reciprocal of the chi square distributions, then let \(X\sim F_{(m,n)}\) hence \(1/X\sim F_{(n,m)}\), so \[\begin{align} \alpha =& P\left(X\le F_{\alpha, (m,n)}\right)\\ =& P\left(1/X \ge 1/F_{a, (m,n)} \right)\\ =& 1 - P\left(1/X \le 1/F_{a, (m,n)} \right)\\ =&1-P\left( F_{(n,m)} \le 1/F_{a, (m,n)}\right)\\ =&1-F_{(n,m)}(1/F_{a, (m,n)}) \end{align}\] thus, \[\begin{align} 1-\alpha =& F_{(n,m)}(1/F_{a, (m,n)})\\ F_{1-\alpha, (n,m)} =& 1/F_{a, (m,n)}. \end{align}\]

If \(X\sim t_q\), then \(X^2\sim F_{1,q}\)

A random variable \(X\) has a standard Student’s \(t\) distribution with \(q\) degrees of freedom if it can be written as a ratio \[T=\frac{N(0,1)}{\sqrt{\chi^2_q/q}}\]between a standard normal random variable \(Z\sim N(0,1)\) and a Chi-square random variable with \(v\) degrees of freedom divided by \(q\), which is independent of \(N(0,1)\).

then \(X^2=\frac{Z^2/1}{\chi^2_q/q}\sim F_{1,q}\)

Exercise 4.7.13. Suppose we generate a random variable \(X\) in the following way. First we flip a fair coin. If the coin is heads, take \(X\) to have a \(\text{Uniform}(0, 1)\) distribution. If the coin is tails, take \(X\) to have a \(\text{Uniform}(3, 4)\) distribution.

(a) Find the mean of \(X\).

(b) Find the standard deviation of \(X\).

Solution. We have \(X = C U_1 + (1 - C)U_2\), where \(U \sim \text{Bernoulli}(1/2)\), \(U_1 \sim \text{Uniform}(0, 1)\) and \(U_2 \sim \text{Uniform}(3,4)\) are all independent.

(a)

\[\mathbb{E}(X) = \mathbb{E}(CU_1 + (1 - C)U_2) = \mathbb{E}(C)\mathbb{E}(U_1) + (1 - \mathbb{E}(C))\mathbb{E}(U_2) = \frac{1}{2} \left(\frac{1}{2} + \frac{7}{2}\right) = 2\]

(b)

\[ X^2 = (CU_1 + (1 - C)U_2)^2 = C^2U_1^2 + (1 - C)^2 U_2^2 + 2C(1 - C)U_1U_2 = C^2U_1^2 + (1 - C)^2 U_2^2 \]

so

\[ \begin{align} \mathbb{E}(X^2) &= \mathbb{E}(C^2)\mathbb{E}(U_1^2) + \mathbb{E}((1 - C)^2) \mathbb{E}(U_2^2) \\ &= \mathbb{E}(C) \mathbb{E}(U_1^2) + \mathbb{E}(1 - C) \mathbb{E}(U_2^2) \\ &= \frac{1}{2} \left( \frac{1}{3} + \frac{37}{3} \right) = \frac{19}{3} \end{align} \]

and then

\[ \mathbb{V}(X) = \mathbb{E}(X^2) - \mathbb{E}(X)^2 = \frac{19}{3} - 2^2 = \frac{7}{3} \]

and so the standard deviation is \(\sqrt{\mathbb{V}(X)} = \sqrt{7/3}\).

Exercise 4.17.14. Let \(X_1, \dots, X_m\) and \(Y_1, \dots, Y_n\) be random variables and let \(a_1, \dots, a_m\) and \(b_1, \dots, b_n\) be constants. Show that

\[ \text{Cov}\left( \sum_{i=1}^m a_i X_i , \sum_{j=1}^n b_j Y_j \right) = \sum_{i=1}^m \sum_{j=1}^n a_i b_j \text{Cov}(X_i, Y_j) \]

Solution. We have:

\[ \begin{align} \text{Cov}\left(\sum_{i=1}^m a_i X_i, Y\right) &= \mathbb{E}\left(\left( \sum_{i=1}^m a_i X_i \right) Y\right) - \mathbb{E}\left( \sum_{i=1}^m a_i X_i \right) \mathbb{E}(Y) \\ &= \sum_{i=1}^m \mathbb{E}(a_i X_i Y) - \left( \sum_{i=1}^m a_i \mathbb{E}(X_i) \right) \mathbb{E}(Y) \\ &= \sum_{i=1}^m \big(\mathbb{E}(a_i X_i Y) - a_i \mathbb{E}(X_i) \mathbb{E}(Y)\big) \\ &= \sum_{i=1}^m a_i \text{Cov}(X_i, Y) \end{align} \]

and, since \(\text{Cov}(A, B) = \text{Cov}(B, A)\),

\[ \text{Cov}\left(X, \sum_{j=1}^n b_j Y_j \right) = \sum_{j=1}^n b_j \text{Cov}(X, Y_j) \]

Applying this for each \(X_i\), we get the result.

Exercise 4.17.15. Let

\[ f_{X, Y} = \begin{cases} \frac{1}{3} (x + y) &\text{if } 0 \leq x \leq 1, 0 \leq y \leq 2 \\ 0 &\text{otherwise} \end{cases}\]

Find \(\mathbb{V}(2X - 3Y + 8)\).

Solution. Let \(r(x, y) = 2x - 3y\). Then:

\[ \mathbb{V}(2X - 3Y + 8) = \mathbb{V}(2X - 3Y) = \mathbb{V}(r(X, Y)) \]

Calculating the expectation of \(r(X, Y)\) and \(r(X, Y)^2\):

\[ \mathbb{E}(r(X, Y)) = \int_0^1 \int_0^2 r(x, y) f(x, y) dy dx = \int_0^1 \int_0^2 \frac{1}{3}(2x - 3y)(x + y) dy dx\\ = \int_0^1 \frac{2}{3}(2x^2 - x - 4) dx = -\frac{23}{9} \]

and

\[ \mathbb{E}(r(X, Y)^2) = \int_0^1 \int_0^2 r(x, y)^2 f(x, y) dy dx = \int_0^1 \int_0^2 \frac{1}{3}(2x - 3y)^2(x + y) dy dx \\ = \int_0^1 \frac{4}{3}(2x^3 - 4x^2 - 2x + 9) dx = \frac{86}{9} \]

and so

\[ \mathbb{V}(r(X, Y)) = \mathbb{E}(r(X, Y)^2) - \mathbb{E}(r(X, Y))^2 = \frac{86}{9} - \frac{23^2}{9^2} = \frac{245}{81} \]

Exercise 4.17.16. Let \(r(x)\) be a function of \(x\) and let \(s(y)\) be a function of \(y\). Show that

\[ \mathbb{E}(r(X) s(Y) | X) = r(X) \mathbb{E}(s(Y) | X) \]

Also, show that \(\mathbb{E}(r(X) | X) = r(X)\).

Solution. We have:

\[ \mathbb{E}(r(X) s(Y) | X = x) = \int r(x) s(y) f(x, y) dy = r(x) \int s(y) f(x, y) dy = r(x) \mathbb{E}(s(Y) | X = x) \]

and so the random variable \(\mathbb{E}(r(X) s(Y) | X)\) takes the same value as the variable \(r(X) \mathbb{E}(s(Y) | X)\) for each \(X = x\) – therefore the random variables are equal.

In particular, when \(s(y) = 1\) for all \(y\), we have \(\mathbb{E}(r(X) | X) = r(X)\).

Exercise 4.17.17. Prove that

\[ \mathbb{V}(Y) = \mathbb{E} \mathbb{V} (Y | X) + \mathbb{V} \mathbb{E} (Y | X) \]

Hint: Let \(m = \mathbb{E}(Y)\) and let \(b(x) = \mathbb{E}(Y | X = x)\). Note that \(\mathbb{E}(b(X)) = \mathbb{E} \mathbb{E}(Y | X) = \mathbb{E}(Y) = m\). Bear in mind that \(b\) is a function of \(x\). Now write

\[\mathbb{V}(Y) = \mathbb{E}((Y - m)^2) = \mathbb{E}(((Y - b(X)) + (b(X) - m))^2)\]

Expand the square and take the expectation. You then have to take the expectation of three terms. In each case, use the rule of iterated expectation, i.e. \(\mathbb{E}(\text{stuff}) = \mathbb{E}(\mathbb{E}(\text{stuff} | X))\).

Solution. We have:

\[ \begin{align} \mathbb{V}(Y) &= \mathbb{E}(Y^2) - \mathbb{E}(Y)^2 \\ &= \mathbb{E}(\mathbb{E}(Y^2 | X)) - \mathbb{E}(\mathbb{E}(Y | X))^2 \\ &= \mathbb{E}\left( \mathbb{V}(Y | X) + \mathbb{E}(Y | X)^2 \right) - \mathbb{E}(\mathbb{E}(Y | X))^2 \\ &= \mathbb{E}(\mathbb{V}(Y | X)) + \left( \mathbb{E}(\mathbb{E}(Y | X)^2) - \mathbb{E}(\mathbb{E}(Y | X))^2 \right) \\ &= \mathbb{E} (\mathbb{V}(Y | X) + \mathbb{V}(\mathbb{E}(Y | X)) \end{align} \]

Exercise 4.17.18. Show that if $(X | Y = y) = c $ for some constant \(c\) then \(X\) and \(Y\) are uncorrelated.

Solution. We have:

\[ \mathbb{E}(XY) = \int \mathbb{E}(XY | Y = y) dF_Y(y) = \int y \mathbb{E}(X | Y = y) dF_Y(y) = \int cy dF_Y(y) = c \; \mathbb{E}(Y)\]

and

\[ \mathbb{E}(X) = \mathbb{E}(\mathbb{E}(X | Y)) = \mathbb{E}(c) = c \]

so \(\mathbb{E}(XY) = \mathbb{E}(X) \mathbb{E}(Y)\), and so \(\text{Cov}(X, Y) = 0\), and so \(X\) and \(Y\) are uncorrelated.

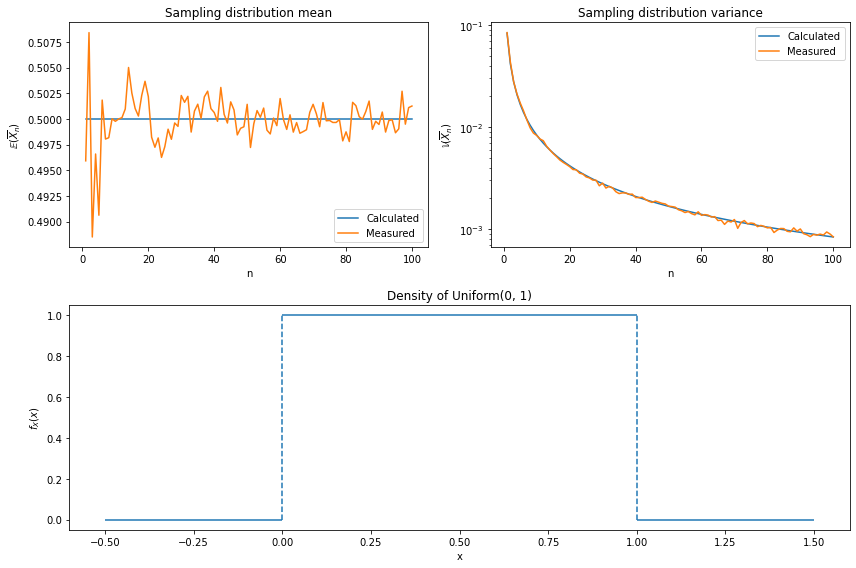

Exercise 4.17.19. This question is to help you understand the idea of sampling distribution. Let \(X_1, \dots, X_n\) be IID with mean \(\mu\) and variance \(\sigma^2\). Let \(\overline{X}_n = n^{-1}\sum_{i=1}^n X_i\). Then \(\overline{X}_n\) is a statistic, that is, a function of the data. Since \(\overline{X}_n\) is a random variable, it has a distribution. This distribution is called the sampling distribution of the statistic. Recall from Theorem 4.16 that \(\mathbb{E}(\overline{X}_n) = \mu\) and \(\mathbb{V}(\overline{X}_n) = \sigma^2 / n\). Don’t confuse the distribution of the data \(f_X\) and the distribution of the statistic \(f_{\overline{X}_n}\). To make this clear, let \(X_1, \dots, X_n \sim \text{Uniform}(0, 1)\). Let \(f_X\) be the density of the \(\text{Uniform}(0, 1)\). Plot \(f_X\). Now let \(\overline{X}_n = n^{-1} \sum_{i=1}^n X_i\). Find \(\mathbb{E}(\overline{X}_n)\) and \(\mathbb{V}(\overline{X}_n)\). Plot them as a function of \(n\). Comment. Now simulate the distribution of \(\overline{X}_n\) for \(n = 1, 5, 25, 100\). Check the simulated values of \(\mathbb{E}(\overline{X}_n)\) and \(\mathbb{V}(\overline{X}_n)\) agree with your theoretical calculations. What do you notice about the sampling distribution of \(\overline{X}_n\) as it increases?

Solution.

\[ \mathbb{E}\left(\overline{X}_n\right) = \mathbb{E}\left(n^{-1} \sum_{i=1}^n X_i \right) = n^{-1} \sum_{i=1}^n \mathbb{E}(X_i) = \frac{1}{2} \]

and

\[ \mathbb{V}\left(\overline{X}_n\right) = \mathbb{V}\left(n^{-1} \sum_{i=1}^n X_i \right) = n^{-2} \sum_{i=1}^n \mathbb{V}(X_i) = \frac{1}{12 n} \]

import numpy as np

np.random.seed(0)

B = 1000

E_overline_X = np.empty(100)

V_overline_X = np.empty(100)

for n in range(1, 101):

X_n = np.random.uniform(low=0, high=1, size=(B, n)).mean(axis=1)

E_overline_X[n - 1] = X_n.mean()

V_overline_X[n - 1] = X_n.var()import matplotlib.pyplot as plt

%matplotlib inline

plt.figure(figsize=(12, 8))

ax = plt.subplot(212)

ax.hlines(0, xmin=-0.5, xmax=0, color='C0')

ax.hlines(1, xmin=0, xmax=1, color='C0')

ax.hlines(0, xmin=1, xmax=1.5, color='C0')

ax.vlines([0, 1], ymin=0, ymax=1, color='C0', linestyle='dashed')

ax.set_xlabel('x')

ax.set_ylabel(r'$f_X(x)$')

ax.set_title('Density of Uniform(0, 1)')

nn = np.arange(1, 101)

ax = plt.subplot(221)

ax.plot(nn, 1/2 * np.ones(100), label='Calculated')

ax.plot(nn, E_overline_X, label='Measured')

ax.set_xlabel('n')

ax.set_ylabel(r'$\mathbb{E}(\overline{X}_n)$')

ax.set_title('Sampling distribution mean')

ax.legend(loc='lower right')

ax = plt.subplot(222)

ax.plot(nn, 1 / (12 * nn), label='Calculated')

ax.plot(nn, V_overline_X, label='Measured')

ax.set_xlabel('n')

ax.set_yscale('log')

ax.set_ylabel(r'$\mathbb{V}(\overline{X}_n)$')

ax.set_title('Sampling distribution variance')

ax.legend(loc='upper right')

plt.tight_layout()

plt.show()

png

Calculated and simulated values agree.

Exercise 4.17.20. Prove Lemma 4.20.

If \(a\) is a vector and \(X\) is a random vector with mean \(\mu\) and variance \(\Sigma\) then

\[ \mathbb{E}(a^T X) = a^T \mu \quad \text{and} \quad \mathbb{V}(a^T X) = a^T \Sigma a \]

If \(A\) is a matrix then

\[ \mathbb{E}(A X) = A \mu \quad \text{and} \quad \mathbb{V}(AX) = A \Sigma A^T \]

Solution.

We have:

\[ \mathbb{E}(a^T X) = \begin{pmatrix} \mathbb{E}(a_1 X_1) \\ \mathbb{E}(a_2 X_2) \\ \cdots \\ \mathbb{E}(a_k X_k) \end{pmatrix} = \begin{pmatrix} a_1 \mathbb{E}(X_1) \\ \mathbb{E}(X_2) \\ \cdots \\ \mathbb{E}(X_k) \end{pmatrix} = a^T \mu \]

and

\[ \mathbb{V}(a^T X) = \mathbb{E}((a^T (X - \mu) (a^T(X - \mu))^T) = \mathbb{E}((a^T (X - \mu) (X - \mu)^T a) = a^T \Sigma a \]

Similarly, for the matrix case,

\[ \mathbb{E}(AX) = \begin{pmatrix} \mathbb{E}\left( \sum_{j=1}^k a_{1, j} X_j \right) \\ \mathbb{E}\left( \sum_{j=1}^k a_{2, j} X_j \right) \\ \cdots \\ \mathbb{E}\left( \sum_{j=1}^k a_{k, j} X_j \right) \\ \end{pmatrix} = \begin{pmatrix} \sum_{j=1}^k a_{1, j} \mathbb{E}(X_j) \\ \sum_{j=1}^k a_{2, j} \mathbb{E}(X_j) \\ \cdots \\ \sum_{j=1}^k a_{k, j} \mathbb{E}(X_j) \\ \end{pmatrix} = A \mu \]

and

\[ \mathbb{V}(A X) = \mathbb{E}((A (X - \mu) (A(X - \mu))^T) = \mathbb{E}((A (X - \mu) (X - \mu)^T A^T) = A \Sigma A^T \]

4.8 Negative binomial (or gamma-Poisson) distribution and gene expression counts modeling

4.8.1 The negative integer exponents binomials

The binomial theorem for positive integer exponents \(n\) can be generalized to negative integer exponents. This gives rise to several familiar Maclaurin series with numerous applications in calculus and other areas of mathematics.

The negative in the name stem from binomial with negative integer exponents. When the binomial has negative integer exponents, such as \[f(x)=(1+x)^{-3}\] we can expand it as a Maclaurin series. The Maclaurin series for \(f(x)\), wherever it converges, can be expressed as \[f(x)=f(0)+f'(0)x+\frac{f''(0)}{2!}x^2+\cdots+\frac{f^{(k)}(x)}{k!}x^k+\cdots\] Since \[f^{(k)}(x)=-3\cdot-4\cdots(-3-k+1)(1+x)^{-3-k}\] then \[f^{(k)}(0)=-3\cdot-4\cdots(-3-k+1)(1+0)^{-3-k}=-3\cdot-4\cdots(-3-k+1)\] So the Maclaurin series becomes \[f(x)=1-3x+\frac{-3\cdot-4}{2!}x^2+\cdots+\frac{-3\cdot-4\cdots(-3-k+1)}{k!}x^k+\cdots\] This converges for \(|x|<1\) by the ratio test.

The above example generalizes immediately for all negative integer exponents \(\alpha\). Let \(\alpha\) be a real number and \(k\) a positive integer. Define \[{\alpha\choose k}=\frac{\alpha(\alpha-1)\cdots(\alpha-k+1)}{k!}=\frac{\alpha!}{k!(\alpha-k)!}\] Let \(n\) be a positive integer. Then \[\begin{align} \frac{1}{(1+x)^n}&=\left(1+x\right)^{-n}\\ &=1-nx+\frac{(-n)(-n-1)}{2}x^2+\cdots+\frac{(-n)(-n-1)\cdots(-n-k+1)}{k!}x^k\\ &=\sum_{k=0}^{\infty}(-1)^k{n+k-1\choose k}x^k \end{align}\] for \(|x|<1\).

Based on the definition of binomial,

\[\begin{align} {x+r-1\choose x}&=\frac{(x+r-1)(x+r-2)\cdots r}{x!}\\ &=(-1)^x\frac{(-x-r+1)(-x-r+2)\cdots (-r)}{x!}\\ &=(-1)^x\frac{(-r-(x-1))(-r-(x-2))\cdots (-r)}{x!}\\ &=(-1)^x\frac{(-r)(-r-1)(-r-2)\cdots (-r-(x-1))}{x!}\\ &=(-1)^x{{-r}\choose x} \end{align}\]

Then

\[\begin{align} 1&=p^rp^{-r}\\ &=p^r(1-q)^{-r}\\ &=p^r\sum_{x=0}^{\infty}{{-r}\choose x}(-q)^{x}\\ &=p^r\sum_{x=0}^{\infty}(-1)^{x}{{-r}\choose x}q^{x}\\ &=\sum_{x=0}^{\infty}{{r+x-1}\choose x}p^rq^{x}\\ &=\sum_{x=0}^{\infty}{{r+x-1}\choose {r-1}}p^r(1-p)^{x}\\ \end{align}\]

4.8.2 The negative binomial distribution derives from the Bernoulli trials and is the sum of i.i.d Geometric distribution

The negative binomial distribution is a discrete probability distribution that models the number of successes (or failures) in a sequence of independent and identically distributed Bernoulli trials before a specified (non-random) number of failures (or successes) (denoted \(r\)) occurs. For example, we can define rolling a \(6\) on a die as a failure, and rolling any other number as a success, and ask how many successful rolls will occur before we see the third failure (\(r = 3\)). In such a case, the probability distribution of the number of non-6s that appear will be a negative binomial distribution. We could similarly use the negative binomial distribution to model the number of days a certain machine works before it breaks down (\(r = 1\)). Or we can model the count number of a specific gene \((x_{iA}, i\in 1,\cdots, M)\) in a library \(A\), \(A\) is the library index. Let \(p\) is the probability of failure (or success) in each trial.

Then \[P_r(X=k)={{k+r-1}\choose{r-1}}(1-p)^kp^{r-1}p={{k+r-1}\choose{r-1}}(1-p)^kp^r\]

Since the Geometric distribution \(P_r(X=k)=p (1 - p)^{k}, k\in (0,\cdots, k+1)\) depicts the number of successes (or failures) (denoted \(k\)) before the first failure (or success), or the total number of trials at the first failure (or success). Then negative binomial distribution is the sum of \(r\) i.i.d Geom.

4.8.3 The Expectation, Variance and Moment-generating function of negative binomial distribution

The Generating Function

By definition, the following is the generating function of the negative binomial distribution, using : \[\begin{align} g(z)&=\sum_{x=0}^{\infty}{{r+x-1}\choose{x}}p^rq^xz^x\\ &=\sum_{x=0}^{\infty}{{r+x-1}\choose{x}}p^r(qz)^x\\ &=p^r\sum_{x=0}^{\infty}(-1)^x{{-r}\choose x}(qz)^x\\ &=p^r\sum_{x=0}^{\infty}{{-r}\choose x}(-qz)^x\\ &=p^r(1-qz)^{-r}\\ &=\frac{p^r}{(1-qz)^{r}}\\ &=\frac{p^r}{(1-(1-p)z)^{r}};\quad z<\frac{1}{1-p}\\ \end{align}\]

The moment generating function of the negative binomial distribution is: \[M(t)=\frac{p^r}{(1-(1-p)e^t)^{r}};\quad t<-\ln(1-p)\]

The Mean:

\[\begin{align} \mathbb E(X)&=g'(1)\\ &=\left(\frac{p^r}{(1-(1-p)z)^{r}}\right)'\bigg|_{z=1}\\ &=\left(\frac{-r(-(1-p))p^r}{(1-(1-p)z)^{r+1}}\right)\bigg|_{z=1}\\ &=\frac{r(1-p)p^r}{p^{r+1}}\\ &=\frac{r(1-p)}{p}\\ \end{align}\]

\[\begin{align} \mathbb V(X)&=\mathbb E(X^2)-(\mathbb E(X))^2\\ &=g''(1)+g'(1)-[g'(1)]^2\\ &=\left(\frac{p^r}{(1-(1-p)z)^{r}}\right)''\bigg|_{z=1}+\frac{r(1-p)}{p}-\left(\frac{r(1-p)}{p}\right)^2\\ &=\left(\frac{-r(-(1-p))p^r}{(1-(1-p)z)^{r+1}}\right)'\bigg|_{z=1}+\frac{r(1-p)}{p}-\left(\frac{r(1-p)}{p}\right)^2\\ &=\left(\frac{r(1-p)p^r}{(1-(1-p)z)^{r+1}}\right)'\bigg|_{z=1}+\frac{r(1-p)}{p}-\left(\frac{r(1-p)}{p}\right)^2\\ &=\frac{r(1-p)^2(r+1)p^r}{p^{r+2}}+\frac{r(1-p)}{p}-\left(\frac{r(1-p)}{p}\right)^2\\ &=\frac{r(1-p)^2(r+1)}{p^2}+\frac{r(1-p)}{p}-\frac{r^2(1-p)^2}{p^2}\\ &=\frac{r(1-p)}{p^2} \end{align}\] and

Since the expectation of geom is \(\mathbb{E}(X)=\frac{1-p}{p}\quad(x=0,1,2,3,\cdots)\quad (\text{or } 1/p \quad x=1,2,3,\cdots)\) and variance of geom is \(\mathbb{V}(X) = \frac{1 - p}{p^2}\), then the negative binomial distribution is the sum of \(r\) i.i.d Geometric.

4.8.4 The connection with Poisson distribution

Since \(\Gamma(a)=(a-1)!\) then \[Pr(X=k)={{k+r-1}\choose{r-1}}(1-p)^kp^r=\frac{\Gamma(k+r)}{k!\Gamma(r)}(1-p)^kp^r,\quad k=0,1,2,\cdots\] denote \(X\sim NB(r,p)\), when \(r\to\infty\) and \(p\to 0\) and \(\mathbb E(X)=\frac{r(1-p)}{p}\) remain constant, let \[\lambda=\frac{r(1-p)}{p}\Rightarrow p=\frac{r}{r+\lambda}\] Then \[\begin{align} Pr(X=k;r,p)&={{k+r-1}\choose{r-1}}(1-p)^kp^r\\ &=\frac{\Gamma(k+r)}{k!\Gamma(r)}(1-p)^kp^r\\ &=\frac{1}{k!}\cdot\frac{\Gamma(k+r)}{\Gamma(r)}\left(\frac{\lambda}{r+\lambda}\right)^k\left(\frac{r}{r+\lambda}\right)^r\\ &=\frac{\lambda^k}{k!}\cdot\frac{\Gamma(k+r)}{\Gamma(r)(r+\lambda)^k}\left(\frac{r}{r+\lambda}\right)^r\\ &=\frac{\lambda^k}{k!}\cdot\frac{\Gamma(k+r)}{\Gamma(r)(r+\lambda)^k}\left(1+\frac{\lambda}{r}\right)^{-r}\\ &=\frac{\lambda^k}{k!}\cdot1\cdot\frac{1}{e^{\lambda}}\\ &=\frac{\lambda^k}{k!e^{\lambda}} \end{align}\] which is Poisson distribution.

4.8.5 Expectation, Variance and overdispersion

\[\mu=\mathbb E(X)=\frac{r(1-p)}{p}\] \[\sigma^2=\mathbb V(X)=\frac{r(1-p)}{p^2}\] the variance can be write as \[\sigma^2=\mu+\frac{1}{r}\mu^2>\mu\] and when \(r\to\infty\), \[\sigma^2=\mu\]. \(\frac{1}{r}\) is called dispersion parameter, which can be used for data overdispersion test (Wald test: \(H_0:\frac{1}{r}=0\))

4.8.6 gamma-poisson mixture distribution

For \(Y|\lambda\sim Pois(\lambda), \lambda\sim Gamma(r_0,b_0)\), then \[\begin{align} P(Y=y)&=\int_{0}^{\infty}P(Y=y|\lambda)f(\lambda)d\lambda\\ &=\int_{0}^{\infty}\frac{e^{-\lambda}\lambda^y}{y!}\frac{b_0^{r_0}}{\Gamma(r_0)}\lambda^{r_0-1}e^{-b_0\lambda}d\lambda\\ &=\frac{b_0^{r_0}}{\Gamma(r_0)y!}\int_{0}^{\infty}e^{-\lambda}\lambda^y\lambda^{r_0-1}e^{-b_0\lambda}d\lambda\\ &=\frac{b_0^{r_0}}{\Gamma(r_0)y!}\int_{0}^{\infty}e^{-\lambda(b_0+1)}\lambda^{y+r_0-1}d\lambda\\ &=\frac{\Gamma(r_0+y)}{\Gamma(r_0)y!}\frac{b_0^{r_0}}{(b_0+1)^{r_0+y}}\int_{0}^{\infty}\frac{1}{\Gamma(r_0+y)}e^{-\lambda(b_0+1)}\lambda^{y+r_0-1}(b_0+1)^{r_0+y}d\lambda\\ &=\frac{\Gamma(r_0+y)}{\Gamma(r_0)y!}\frac{b_0^{r_0}}{(b_0+1)^{r_0+y}}\int_{0}^{\infty}\frac{1}{\Gamma(r_0+y)}e^{-\lambda(b_0+1)}[\lambda(b_0+1)]^{r_0+y}\frac{1}{\lambda}d\lambda\\ &=\frac{\Gamma(r_0+y)}{\Gamma(r_0)y!}\frac{b_0^{r_0}}{(b_0+1)^{r_0+y}}\\ &=\frac{\Gamma(r_0+y)}{\Gamma(r_0)y!}\left(\frac{1}{b_0+1}\right)^y\left(\frac{b_0}{b_0+1}\right)^{r_0}\\ \end{align}\] which is negative binomial distribution.

4.8.6 reparameterized for counting modeling

The number of failures before r-th success, denote by \(k\): \[f(k;r,p)\equiv Pr(X=k)=\frac{\Gamma(k+r)}{k!\Gamma(r)}p^r(1-p)^k\quad k=0,1,2,\cdots\]

\[\mu=\mathbb E(X)=\frac{r(1-p)}{p}\] \[\sigma^2=\mathbb V(X)=\frac{r(1-p)}{p^2}\] Then \[p=\frac{\mu}{\sigma^2}\] \[r=\frac{\mu^2}{\sigma^2-\mu}\]

\[f(k;r,p)\equiv Pr(X=k)={k+\frac{\mu^2}{\sigma^2-\mu}-1\choose{\frac{\mu^2}{\sigma^2-\mu}-1}}\left(\frac{\sigma^2-\mu}{\sigma^2}\right)^k\left(\frac{\mu}{\sigma^2}\right)^{\frac{\mu^2}{\sigma^2-\mu}}\]

The \(\mu\) and \(\sigma^2\) of each gene can be estimated from data.

We assume that the number of reads in sample \(j\) that are assigned to gene \(i\) can be modeled by a negative binomial (NB) distribution,

\[K_{ij}\sim NB(\mu_{ij},\sigma^2_{ij}),\tag1\]

which has two parameters, the mean \(\mu_{ij}\) and the variance \(\sigma^2_{ij}\). The read counts \(K_{ij}\) are non-negative integers. The NB distribution is commonly used to model count data when overdispersion is present.

In practice, we do not know the parameters \(\mu_{ij}\) and \(\sigma^2_{ij}\), and we need to estimate them from the data. Typically, the number of replicates is small, and further modelling assumptions need to be made in order to obtain useful estimates.

- First, the mean parameter \(\mu_{ij}\) , that is, the expectation value of the observed counts for gene \(i\) in sample \(j\), is the product of a condition-dependent per-gene value \(q_{i, \rho(j)}\)(where \(\rho(j)\) is the experimental condition of sample \(j\)) and a size factor \(s_j\),

\[\mu_{ij} = q_{i, \rho(j)}s_j.\tag2\] \(q_{i, \rho(j)}\) is proportional to the expectation value of the true (but unknown) concentration of fragments from gene \(i\) under condition \(\rho(j)\). The size factor \(s_j\) represents the coverage, or sampling depth, of library \(j\), and we will use the term common scale for quantities, such as \(q_{i, \rho(j)}\), that are adjusted for coverage by dividing by \(s_j\).

- Second, the variance \(\sigma^2_{ij}\) is the sum of a shot noise term and a raw variance term,

\[\sigma^2_{ij}=\mu_{ij}+s_j^2v_{i,\rho(j)},\tag3\]

- Third, we assume that the per-gene raw variance parameter \(v_{i,\rho(j)}\) is a smooth function of \(q_{i, \rho(j)}\),